Why You Can’t Just Use the Endowment for That

How Stanford’s billions really work.

Reading time 9 min

By

Kathy Zonana

It’s a common reaction. When the university announces a budget cut, the internet commentariat erupts: Stanford has $27 BILLION in endowment. Why can’t it just dip into it? (The BILLION is invariably rendered in all caps.)

Indeed, $27.7 billion—the value of the endowment as of August 31, 2019—is a lot of money. It is roughly what Americans were projected to spend on Valentine’s Day gifts in 2020. It is a bit more than the gross domestic product of El Salvador. It is $737 for every person in Canada.

It’s also a substantial endowment for a university—in the United States, the only three larger belong to Harvard, Yale and the University of Texas system. But that doesn’t mean Stanford has a ginormous piggy bank. In fact, 90 percent of the endowment—more than 8,000 different funds, plus a certain 8,180 acres of Farmland—is restricted or designated for specific uses. It can’t be spent on anything the university chooses. Here’s why.

The endowment is not a savings account. It’s more like a retirement annuity—for a retiree that’s supposed to live forever.

Look 125 years into the past. There’s Stanford, a fledgling university at age 4. Look 125—or 250 or 500—years into the future. There, one hopes, is Stanford, in robust good health. The university was established with a Founding Grant of lands from Leland and Jane Stanford, and their vision was that the school would exist in perpetuity. In fact, the Founding Grant stipulates that Stanford’s lands can never be sold.

Randy Livingston (Photo: Erin Attkisson)

Randy Livingston (Photo: Erin Attkisson)

The endowment, which now includes invested assets in addition to those lands, "is not simply like a savings account," says Randy Livingston, ’75, MBA ’79, Stanford’s vice president for business affairs and CFO. "It’s the income generated from investing the endowment, not the endowment principal itself, that supports 20 percent of our annual operating budget. If we start to consume the endowment principal, there will be less to invest and therefore less income to support the university in future years."

A better analogy, Livingston says, would be an annuity, "where you’re living off the income and preserving the principal in order to maintain that income over time." That’s all well and good if you’re a human retiree who can look at an actuarial table and figure that the income from your annuity will meet your needs for the next 25 years. But remember, Stanford hopes to live forever, and costs go up over time—largely because about two-thirds of the university’s expenses are compensation for faculty and staff, and the cost of living in the Bay Area is high. So in order not to reduce the buying power of the endowment, the university needs to reinvest rather than spend some of the income it generates.

Which leaves the portion of the endowment income that Stanford withdraws each year to support its operations. That’s called the payout, and it came to more than $1.3 billion in 2019–20. "Endowment payout funds every university activity, including a substantial part of undergraduate and graduate education and research," says Livingston.

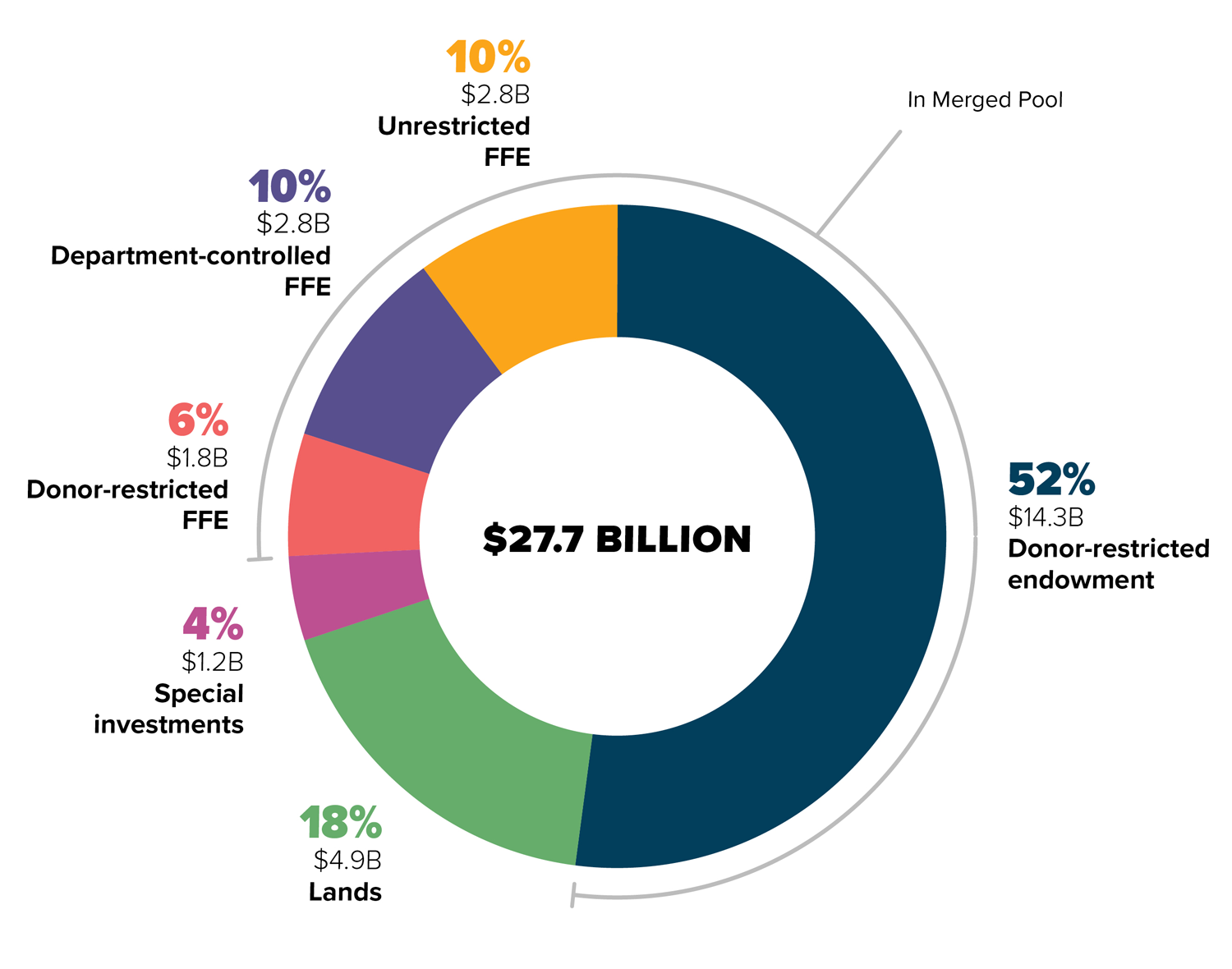

The Endowment (2019)

Figures add to more than $27.7 billion because of rounding.

Figures add to more than $27.7 billion because of rounding.

Almost 80 percent of the endowment is invested in the Merged Pool, which is the university’s primary investment fund. We’ll dive more deeply into the pool later, but for now, just know that it operates similarly to a mutual fund, where each of more than 8,000 endowment funds holds shares of the Merged Pool and it pays out income annually on a per-share basis. The university projects an average 9 percent annual return on the Merged Pool, understanding, of course, that any given annual return may deviate substantially from that average—so it uses a smoothing formula to mitigate the impact of investment volatility. In a typical budget year, Stanford targets payout of approximately 5.5 percent, generally leaving 3.5 percent to reinvest so that the endowment principal keeps pace with the average rise in costs. Unless—well, unless it’s now.

A benefactor might donate funds to cover a public-interest law professor’s salary and benefits in perpetuity. That’s part of the endowment.

"Most years, the trustees use the smoothing formula to determine the payout," says Livingston. "However, during periods of extreme market volatility, the trustees use their discretion and may deviate from the smoothing formula. Investment markets were extremely volatile in spring 2020 when trustees were making the fiscal-year ’21 payout decision." If they had followed the smoothing formula, the payout would increase by 3 percent in 2020-21. But that seemed like a worrisome course. "The COVID-19 pandemic was still unfolding, with huge economic uncertainty about the year ahead," Livingston says. "Trustees were concerned about the likelihood of a significant investment downturn, similar to 2008-09." So they took a conservative approach, applying the 3 percent increase only to endowment funds supporting student aid. For all other endowment funds, the trustees decided to reduce payout by 10 percent.

Wait—there are specific funds for specific things, like financial aid? Oh, you bet there are. Let’s take a closer look.

The endowment is not a monolith. It’s actually a whole bunch of little endowments. The vast majority of the endowment is restricted—meaning it’s made up of assets that can only be used for the purpose for which they were contributed.

Let’s start with the biggest category: restricted gifts. "The endowment" includes more than 7,000 gifts that were made at different times for different purposes. For example, a benefactor might donate funds to cover a public-interest law professor’s salary and benefits in perpetuity. That’s part of the endowment. So are a lot of undergraduate scholarships, graduate fellowships and research funds. Together, they total 52 percent of the endowment. And some of them are pretty detailed.

One scholarship is for a football player majoring in civil engineering; another for the one who wears No. 36. One fellowship is limited to "medical students who are graduates of a public or parochial school located in Des Moines, Iowa, or if there is no such qualified student to a graduate of any school in the State of Iowa." Another states a preference for students born, raised or educated in Montana, North Dakota or Thailand.

So that’s a little more than half of the endowment pie. The other slices are smaller and a bit more complicated. The smallest one (4 percent of total endowment) is made up of specially managed venture and investment funds, each set up to support a school or unit—Graduate School of Business; Stanford Earth; the Department of Athletics, Physical Education and Recreation; and so forth. Then there are three groups of "funds functioning as endowment" (FFE): donor-restricted FFE (6 percent of the total endowment); department-controlled FFE (10 percent of the total); and unrestricted, centrally controlled FFE (another 10 percent). Donor-restricted FFE and department-controlled FFE operate similarly to restricted gifts—their payout is not fungible. So, for example, if a donor-restricted endowment fund to purchase phonograph records generates payout that is reinvested as FFE, the payout from that FFE cannot later be used to purchase musical instruments. Or if the geophysics department converts a large expendable gift to FFE, that payout can’t later be deployed on behalf of the philosophy department.

Which brings us to the unrestricted, centrally controlled FFE. This 10 percent slice provides valuable discretionary income to the university. About two-thirds of its payout flows to general funds that the provost allocates to everything from academic departments to libraries to financial aid to facilities. The remaining one-third is allocated by the president for strategic initiatives, such as the university’s long-range vision.

Oh, and don’t forget those Stanford lands that make up 18 percent of the endowment. They can’t be sold, but they can be leased.

"I think one of the very cool things is that the original endowment of the university—what Leland and Jane Stanford gifted to us—was the 8,000-plus acres of the Stanford campus, a portion of which we have been able to use to generate income through the Stanford Research Park, the Stanford Shopping Center and the Sand Hill Road properties, and that is a component of the endowment that has actually grown dramatically in value over the last five to 10 years with the continued growth of Silicon Valley and the surrounding community-derived property values," says Livingston. "It’s very unique to Stanford, as compared with any of our peers, having the land as a major part of the endowment as a service that continues to provide income to us."

When a parcel of land is leased for a long time—30 to 50 years—the prepaid revenue from that lease is added to the Land Development Fund, which is centrally controlled FFE and is used, for example, to redevelop properties in the Stanford Research Park. Meanwhile, the net annual rent the university collects—$93 million in 2018–19—is unrestricted endowment payout that flows into general funds.

To go deeper, you have to dive into the pool (and learn the meaning of the term buffer).

The bulk of the endowment—everything but the lands and the special investments—is overseen by Stanford Management Company, the university’s investment office, in the Merged Pool, which was valued at $29.6 billion on June 30, 2019. That’s close to the GDP of Nepal, by the way.

As its name suggests, the Merged Pool (the mutual fund) contains several different types of assets, including endowment funds (the annuity), expendable funds (think of this more like a set of checking accounts) and hospital funds.

‘The buffers have always been viewed as the unrestricted emergency reserve to help bail us out in the event of an earthquake or a pandemic or some other event like that.’

Now, about those expendable funds. They’re not endowment. Quite the contrary. They can be spent in any given year. But at present, they add up to more than $4 billion, and since 90 percent of them are invested in the Merged Pool, they generate a lot of return on investment. And some of those investment returns—let’s call them "interest" for purposes of our checking-account analogy—become unrestricted funds functioning as endowment. Brace yourself.

"I will say at the outset, it is very complex," Livingston says. The expendable funds pool, he explains, is a collection of reserves and expendable funds across the university—more than 26,000 different accounts. Take your intrepid Stanford Alumni Association: "The Alumni Association has monies that they’ve received in the door each year that they haven’t yet spent, and sometimes those funds carry over from year to year—there’s some mismatch between when monies come in and when they go out," says Livingston. "My organization is the Bank of Stanford, so we treat each of those accounts like checking accounts. The fund holders deposit their money in the central bank. We guarantee their principal—they can draw on those monies anytime they want—but we don’t pay any interest."

Instead, here’s what happens to that "interest": Prior-year investment returns on the expendable funds pool of zero to 5.5 percent flow to the university’s general funds. Anything above 5.5 percent is added to a pair of funds called the buffers. If the return is, say, 10 percent, "that can be several hundred million dollars," says Livingston. And that’s when some of the interest on Stanford’s collection of checking accounts becomes endowment. Remember that 10 percent, $2.8 billion slice of the endowment pie that is unrestricted, centrally controlled FFE? That’s mostly the buffers.

The buffers have four jobs: First, they keep the expendable funds whole in the case of a negative return. "We still have to guarantee the principal of the expendable funds checking accounts," says Livingston, "so we use the buffers to replenish any losses they might have had, and that’s where the term buffer came from." Second, since the buffers themselves are invested as FFE, they provide shares of endowment payout to be allocated by the president and provost, as we talked about in the last section. Third, says Livingston, the buffers serve as "a source of unrestricted capital when nothing else is available." In fact, this is the only portion of the endowment from which the university spends principal when it needs to address pressing financial needs. In recent years, the Board of Trustees has authorized the withdrawal of $500 million from the buffers to address housing affordability issues for graduate students, faculty and staff.

Last but most certainly not least, the buffers serve as an emergency fund. In June, the board authorized the withdrawal of up to $150 million to fund budget shortfalls related to COVID-19. "If we were to have the most severe earthquake that we can imagine close to campus, we have projected that the financial impact of that would be on the order of $4 billion in damages," says Livingston. "The buffers have always been viewed as the unrestricted emergency reserve to help bail us out in the event of an earthquake or a pandemic or some other event like that."

So, yes, Stanford has $27 BILLION in endowment. And, yes, it does, under certain circumstances, tap the principal of the one small slice it can—the buffers. But those circumstances have to be extraordinary.

Kathy Zonana, ’93, JD ’96, is the editor of Stanford. Email her at [email protected].

Stanford is working to address urgent imperatives in the country and the world.

Carl Bergstrom, PhD ’98, has become an interpreter of fallacies.