The Case for Small Multifamily

Why the small multifamily residential class is positioned to pick up where single-family rentals left off

Over the past decade, single-family rentals (SFR) emerged as a significant institutional real estate asset. But the combination of rate hikes and heightened competition has led to a sharp decline in institutional activity in the SFR sector. As a result, investors are increasingly looking to slightly larger properties—small multifamily—for the next big investment opportunity. Today, we’ll explore how and why the small multifamily sector is gaining interest among institutional owners and where it might go from here.

Multifamily real estate has had a complex few years. The disruption caused by the pandemic drove millions of people out of cities, forcing residential landlords, used to consistently climbing rents over the past few decades, to deeply discount their units in order to maintain occupancy. Then renters flooded back, but so did regulatory overhead, mortgage rates, and costs of doing business, from insurance to maintenance and repairs.

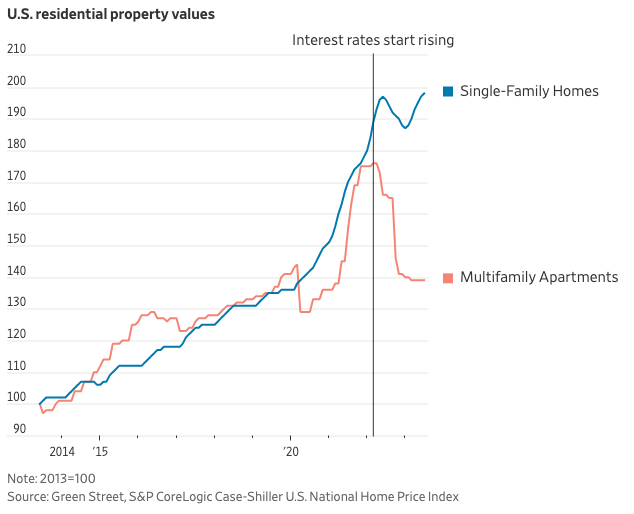

Although demand for urban living began picking up again in 2022, driving rents to new heights in nominal terms, the Federal Reserve’s decision to raise interest rates in response to inflation has made financing/refinancing real estate purchases, whether for owner-occupiers or for investment, significantly more expensive, putting downward pressure on residential real estate values even as rents continue to climb.

As shown in the graph above, trade prices for multifamily real estate have dropped precipitously following rate hikes, while those of single-family homes have continued to climb, albeit more slowly than before the hikes. In large part, this is due to a different buyer pool. Millions of individuals are vying for single-family homes alongside institutional purchasers, whereas primarily institutions, operating under stricter financial return parameters, are active in the multifamily space.

Small buildings, big opportunity

The continued rise of single-family home prices is driving down yields and making scattered-site SFR less attractive to returns-conscious institutional buyers. Cap rates in the space have dropped considerably, and many of the largest players have shifted from being net buyers to net sellers. At the same time, the combination of climbing multifamily rents and stagnant sticker prices suggests a latent opportunity within a broadly undervalued class, but which subset presents the best opportunity along other dimensions?

Broadly speaking, one can divide residential assets into single-family (1 unit), small multifamily (2-50), and large multifamily (>50 units). Larger multifamily assets have traditionally been the core focus of institutional real estate, with single-family representing a recent institutional area of focus. With plenty of supply in SFR and insufficient infrastructure to scalably deploy capital into small multifamily, the small multifamily sector has been largely absent from institutional focus. But it satisfies four relevant criteria that point towards its potential as a candidate for increased institutional focus:

Historically lower-performing/difficult to manage efficiently

Positioned for performance improvement using emerging tech/methods

Experiencing unique stresses as a result of the current economic crisis

Not broadly institutionalized

For example, in a Boston survey of over 17,000 small multifamily rental properties, only 32% were owner-occupied (i.e. most are investment properties) and of the remaining 68%, 88% were owned by groups with three or fewer total properties. This lack of institutional focus and investment has generally relegated small multifamily to a bimodal fate: underinvestment from smaller operators who don’t invest the capital to bring them up to modern environmental and living standards, or condo developers who can turn a three-unit building into two or three higher-end condos with significant investment and a bet on the sale price outpacing the costs of acquisition and upgrade.

From a rental perspective, the size of the small multifamily asset class and the removal of the SFR asset class as a viable institutional investment opportunity presents a market for a next SFR-like asset class. There are over one million 2-20 unit buildings in the United States, which serves as a large base supply for a new asset class, what we call the Modern Urban Rental (MUR). MURs are upgraded experiences in non-amenitized 2-20-unit residential buildings in dense urban cores. Similar to SFR, operators typically upgrade interiors, utilities, and smart systems to improve resident experience, operational efficiency, and environmental sustainability while benefiting from increased rents and lower operating expenses than smaller, less-scaled operators.

Small Multifamily is the new SFR

Small multifamily properties are ubiquitous in cities across the US. They began to spring up en masse in the late 19th and early 20th centuries, driven by the combination of demand for cheap housing from waves of immigrants seeking opportunity in US cities and the absence of the zoning regimes that would soon spring up across the country and restrict further construction of small multifamily properties and other cost-effective housing typologies.

Historically, small multifamily properties have constituted the backbone of naturally occurring affordable housing in otherwise expensive cities. In the second half of the 20th century, broader urban trends in the US contributed to disinvestment in many of these properties even as investment flowed into newer large developments. Nevertheless, recent decades have seen an uptick in demand for all forms of urban housing, resulting in renewed interest in small multifamily properties from residents and investors alike.

Despite this, institutional ownership of small multifamily remains low given the operational challenges they present. Unlike SFRs, these are multi-unit assets, so far more maintenance tasks remain the responsibility of the property operator, not the single tenant user. Unlike large multifamily assets, small multifamily assets cannot rely on centralized, onsite staff who can respond quickly to maintenance requests and perform routine checkups without traveling from property to property. With traditional management practices, this results in significantly higher expense ratios, producing returns that are unattractive to institutional investors.

The MUR Playbook

Fortunately, small multifamily operators have the opportunity to build upon the SFR playbook, borrowing some elements of it while developing other practices from scratch. As with SFR in the wake of the global financial crisis, institutional buyers can take advantage of favorable acquisition conditions driven by the pandemic and its associated economic disruptions. Many tech solutions that were successfully deployed in SFR, including smart locks and remote thermostat controls, are equally applicable to small multifamily. Similarly, data-driven bulk acquisition strategies are viable in both asset classes and necessary to speedily deploy capital with lower per-property analysis and soft costs. Lastly, bundling service calls into geographic clusters and preventive maintenance can drive down operating costs, shaving critical percentage points off of expense ratios.

The first stage of the property lifecycle in which small multifamily operators are making improvements is the acquisition process. Analyst and broker hours aren’t cheap, and when the price tag for a given property is in the low 7-figures, as is true with many small multifamily properties, these costs make a much bigger difference than with large multifamily properties with 8-figure prices.

To economize on these costs, small multifamily operators have built software solutions that automatically filter potential acquisition targets based on a wide variety of criteria that impact their expected performance. Standard factors like unit/room count, square footage, and neighborhood comps play a role, but so do more novel factors derived from large-scale data analysis. For instance, in some cities, inter-sale duration, i.e. the time elapsed since the previous sale of a given property, impacts the degree to which assessed value lags behind market value, creating opportunities for tax arbitrage. Using these factors to narrow the field of acquisition targets results in more efficient use of human analyst time.

Ongoing operating costs can also be mitigated via logistics improvements and onsite solutions. Many of the last-mile logistics techniques pioneered by companies like Uber or Grubhub over the past decade are transferable to maintenance routing for scattered-site real estate portfolios, whether SFR or small multifamily. Employing these techniques alongside preventive maintenance can meaningfully reduce maintenance costs. At Groma, the Boston-based operator of small multifamily properties we co-founded, we’ve found that these practices reduce maintenance costs by up to 20%. Depending on the plumbing layout of a building (another relevant filter for the acquisitions process), metering water separately for each unit can enable water usage to be billed back to tenants, reducing total operating cost by up to 3% and improving environmental outcomes by removing the moral hazard of zero-marginal-cost water use. Additionally, using a standardized set of appliances and materials for building renovation leads both to meaningful supplier discounts and a lower-friction repair process.

Additionally, there are significant costs and challenges to effectively underwriting small multifamily assets. Single-family assets benefit from sophisticated pricing models based on consumer trade prices and rental demand, some of those being so well known and distributed that the average consumer knows how to find a "Zestimate" on any home in the country.

On the institutional side, decades of underwriting practice and tools like CoStar bring similarly sophisticated pricing regimes to large multifamily assets. Additionally, with average trade prices in the tens of millions of dollars, analysts can be hired to sort through the data and underwrite each asset individually.

Small multifamily is a blind spot. The sector has limited consumer price trade data compared to SFR, no sophisticated tooling like CoStar, and trade prices low enough that new tools are required to efficiently underwrite these assets. In Boston alone, roughly 300 "triple-deckers" come on the market in a given month–too many for an analyst to review without machine-driven intelligence assisting them. Many practices developed in the SFR ecosystem can be adjusted and adapted to small multifamily, but many differences also make it not a clean one-to-one translation.

Small Multifamily differs from SFR in key ways

Despite these similarities, the small multifamily asset class differs from SFRs in a number of ways, many of which align with current renter and societal preferences:

Sustainability/walkability: Nearly all small multifamily properties are located in dense, urban areas close to public transit options, as compared to SFRs, which are generally found in lower-density suburbs/exurbs. This results in lower carbon emissions and traffic congestion attributable to small multifamily. Additionally, small multifamily has lower average unit sizes and shared walls, meaning that the energy needed to heat and cool them is also substantially lower.

Preserving homeownership opportunities: Institutional ownership of SFRs has been criticized for taking homeownership opportunities away from individual buyers. While this narrative is often exaggerated–institutional investors only own 25% of SFRs, or 6% of all single-family homes in the US–it doesn’t hurt that, on the margin, institutional ownership of small multifamily preserves affordable rental opportunities without reducing the stock of homes available for individual ownership. This also reduces the likelihood of politicians threatening to punish the small multifamily industry via regulation.

Regulatory environment: A corollary to small multifamily properties being located primarily in older cities and SFRs being located primarily in newly developed suburban areas is that the predominant regulatory environments affecting the two classes differ greatly. Old cities like New York, San Francisco, and Boston are both highly restrictive in terms of their attitudes toward new development and present a wide variety of regulatory challenges for landlords. Newer suburban areas in the Sunbelt are the opposite, with favorable attitudes towards development and relatively straightforward policies regarding landlord/tenant relations. This contrast creates favorable conditions for large institutional landlords who operate small multifamily assets: the market value of their assets is buffered by the difficulty of adding new supply, and the complexity of tenant law gives them a competitive advantage relative to smaller operators who can’t invest in standardized compliance processes to the same degree.

More Small Multifamily, Less SFR

A widely cited report from MetLife predicts that institutions will own 40% of SFRs by 2030. There are two ways for that metric to be true. One is that the SFR market will continue to grow, with institutions playing a larger role. MetLife projects that 7.6 million single-family homes will be SFRs by 2030. The second, which we believe is more likely, is that a number of trends will cause the overall SFR market to stagnate or shrink, with institutions owning a larger part of the smaller total:

Institutional buyer saturation: Institutional ownership of single-family assets grew quickly over the past decade, but the rate of increase has fallen dramatically over the past year. This is the standard logistic growth pattern: new entrants expand rapidly as they consume the low-hanging fruit, but their growth is naturally limited as competitors enter the market and as the most appealing opportunities are exhausted, resulting in a stable equilibrium at a higher level.

Individual buyer competition: When interest rates begin to drop as expected, individual buyers who have been delaying home purchases will re-enter the market with gusto, bidding up prices even further out of reach for returns-conscious institutional acquisitions teams. This exuberance from individual buyers makes sense. Given the advantaged mortgage programs, tax subsidies, and cultural desire for homeownership, individuals should be willing to "overpay" for a home compared to an institutional buyer viewing it simply as a financial asset.

Political pressure: With continuing scrutiny over institutional ownership of single-family homes, many asset-class-agnostic capital allocators may prefer to focus on investments that are not seen as taking homeownership opportunities off of the table in order to avoid political backlash.

Based on the trends described in this report, we believe effective SFR cap rates will trend below those of small multifamily, and eventually below those of large multifamily, due to overwhelming demand and government subsidies for individual homeowners. This will price out institutional owners.

SFR, small multifamily, and multifamily cap rates. Historical data sourced from Arbor Realty and Chandan Economics, projections from Groma Research.

Excess institutional capital, searching for yield and in-demand residential assets, will be redirected to new asset classes, such as small multifamily, which is still recovering from the unique stresses that impacted them during the pandemic. Current institutional ownership of the small multifamily asset class is de minimis and not widely tracked, similar to SFR in 2010. However, we predict that institutional ownership of this asset class will grow from current untracked levels to 20-25% by 2030, which would make small multifamily an institutional asset class consisting of hundreds of thousands of buildings and millions of units.

Many asset allocators are currently hesitant to deploy into real estate given uncertainty regarding interest rates, bond yields, and the broader macro environment. These concerns are legitimate–predicting the exact moment at which a given investment becomes the correct decision is inherently difficult. Nevertheless, we believe that as the market turns, the small multifamily asset class is primed to be a key area of focus in this next cycle.

—Chris Lehman and Seth Priebatsch

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them

| A guest post by

|

| A guest post by

|

Start Writing

Start Writing