The Banking Crisis and Its Impact on Small to Midsize Developers

Rising rates and high-profile bank failures have led to an unprecedented pullback in lending. How should real estate operators navigate?

Share this post with a friend

Since you liked this post, why not share it to help spread the word?

Thesis Driven dives deep into emerging themes and real estate operating models. This week is a guest letter from Atif Qadir, the Co-Founder and Chief Impact Officer at Commonplace. It puts the 2023 banking crisis in context and explores its impact on small to midsize developers.

"It is a bad time to be small, whether you are a bank or a company in America."

— Rebecca Patterson, former Chief Strategy Officer at Bridgewater Associates

Entrepreneurial, bootstrapping, pioneering. Small-scale enterprise is the backbone of the American economy. However, businesses of all types and sizes everywhere need access to capital to survive and thrive. This has been the case since the days of the earliest corporations, such as the Dutch East India Company, which financed global trading voyages. Real estate businesses, including small to midsize developers, are no different.

Real estate development is defined by the capital stack, the collection of financing sources used to fund a project. Sometimes a project’s capital stack is filled with debt, covering almost 100% of the project’s cost. In tepid economies, that number comes down to around 50-60%. In major recessions that percentage comes down even further. In any case, understanding debt—and how to get it—is a critical part of getting projects going and staying afloat across real estate cycles.

Right now, we are in the perfect storm of banking industry change, inflation, record high interest rates, a once in a generation change in how we use buildings, and a housing shortage of critical levels, according to Professor Tomasz Piskorski of Columbia Business School. During times of incredible capital markets instability, real estate developers are facing an unprecedented challenge when it comes to accessing debt.

This article maps the ecosystem of debt providers for commercial real estate, explains how this relates to the current and past banking crises, predicts what to expect in the months ahead and relays tips about how to manage downside risk and maximize upside as a small to midsize developer looking for commercial real estate debt.

Background

Commercial Real Estate (CRE) debt comes from 6 primary sources:

Community and regional banks - Community and regional banks provide a third of all CRE debt in the country, and they have an outsized share of small balance debt and office and retail debt. A great example of a regional bank is Provident Bank, which operates in New Jersey, southern New York, and eastern Pennsylvania (disclosure: the author is an Advisory Council member).

Wall Street banks - Major banks like JP Morgan Chase typically service larger balance loans. As a percentage of their deposits, these banks provide less CRE debt than their smaller rivals. Some have special divisions that provide lending services to affordable housing and impact driven projects, like the Community Banking Division at JP Morgan Chase.

Insurance companies - Insurance companies, including "Lifecos" like MetLife are active non-bank lenders. They are able to leverage their massive balance sheets and long-term horizons to provide CRE debt, often at preferential terms for projects that don’t raise red flags using traditional risk metrics.

Community Development Financial Institutions (CDFIs) - CDFIs are government-chartered lending institutions that typically offer lower rates and more flexible terms. There are currently 1,400 such organizations around the country, like Solar and Energy Loan Fund (SELF), a non-bank CDFI based in southeastern Florida that is driving capital to the twin problems of housing affordability and climate resilience. Carver Federal Savings Bank in Brooklyn is an example of a bank CDFI.

Private funds - These non-bank lenders capitalize using an array of sources from high net worth individuals to pensions funds and sovereign wealth funds, and are filling a larger role in riskier debt, such as pre-development, acquisition and bridge financing. An example on the smaller end is Seneca Village Capital, a minority-owned private fund in Harlem. On the larger side are mortgage REITs like Arbor Realty Trust.

Governments and government sponsored enterprises - Federal, state and local government entities like the US Department of Housing and Urban Development and government sponsored enterprises like Fannie Mae are major non-bank CRE lenders, especially for high-leverage and non-recourse construction and permanent debt.

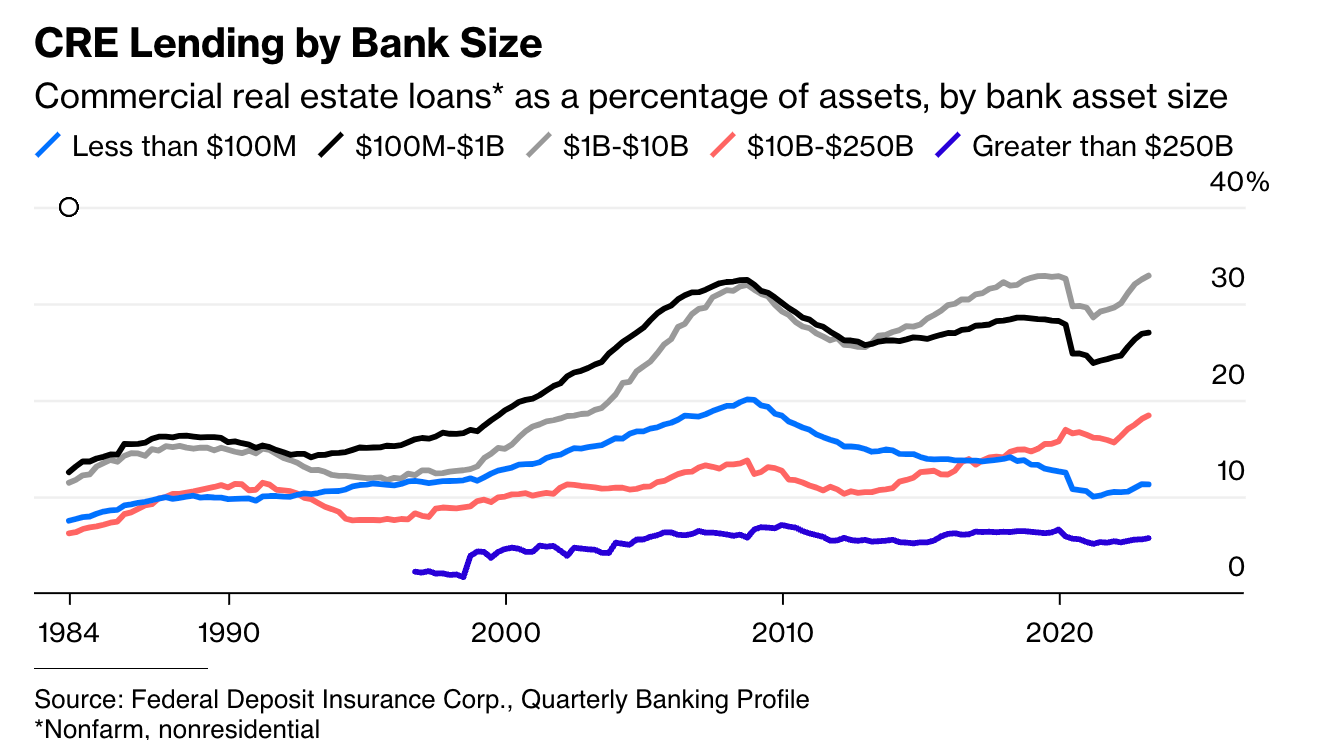

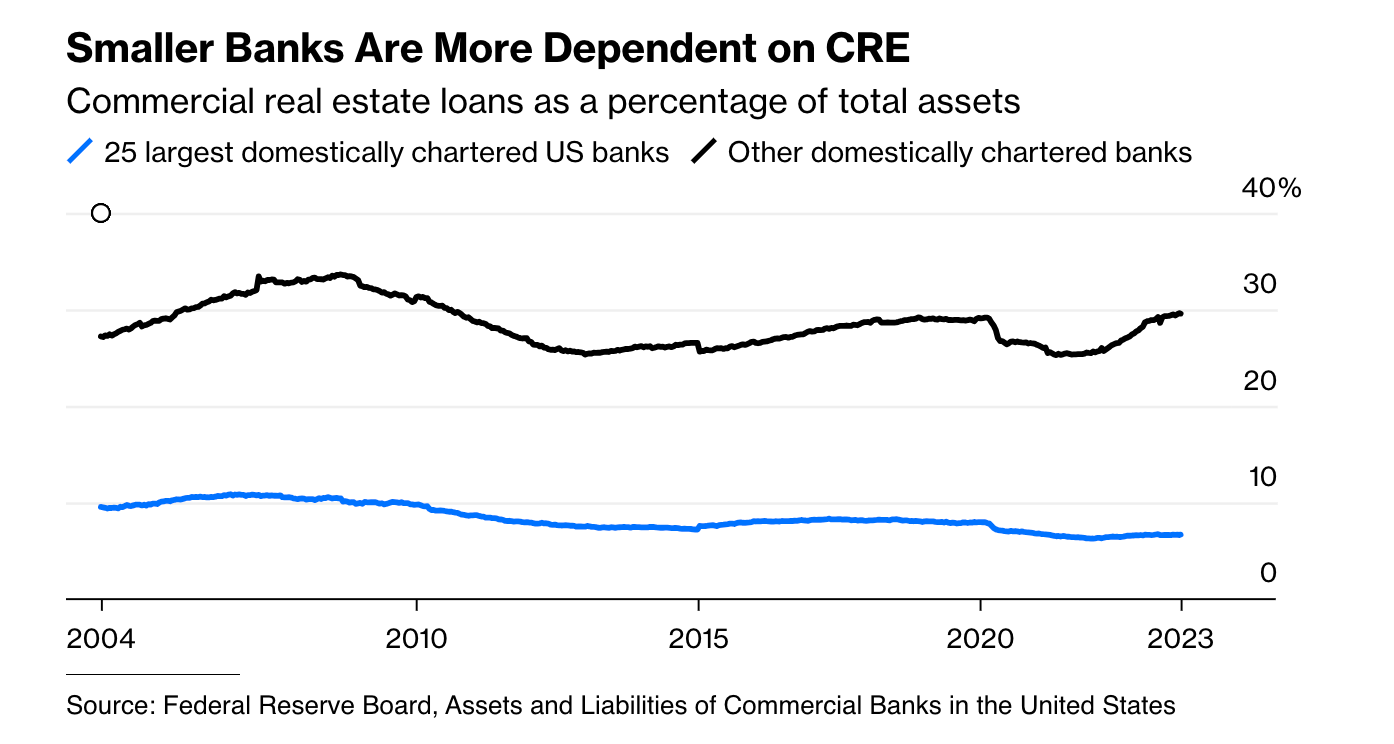

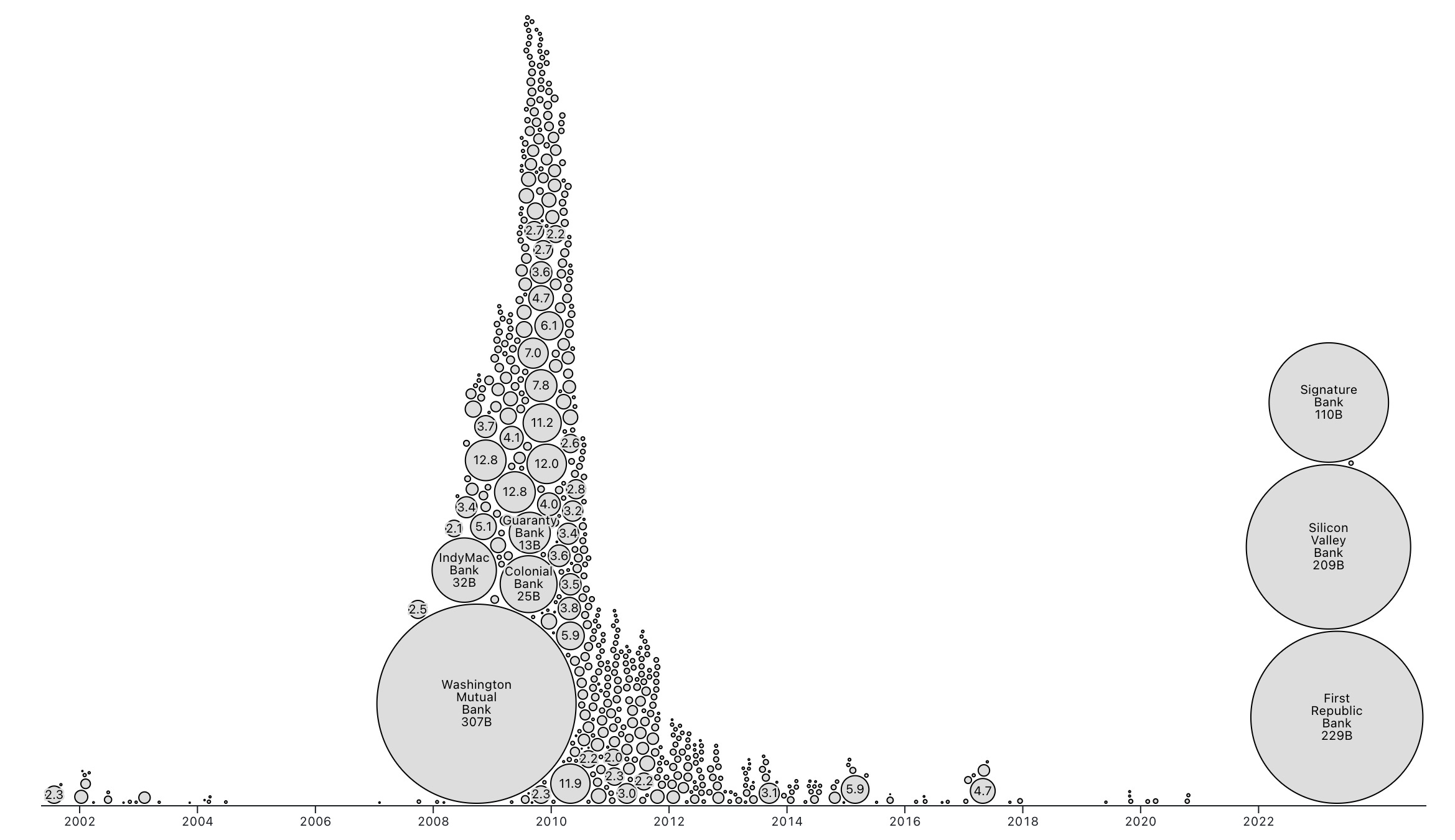

The banking crisis of 2023 highlighted the critical role that community and regional banks play in providing debt for the real estate industry. A lot has been written about these banks (this article by Stacy Cowley for the New York Times is particularly good) but not a lot has been written about these banks’ exposure to commercial real estate. For example, 15% of Silicon Valley Bank’s loan portfolio was in CRE. Signature Bank was a major buyer of Low Income Housing Tax Credits. First Republic Bank held $34B in CRE debt and was a top multifamily lender in San Francisco. And they are not the only ones active in this space:

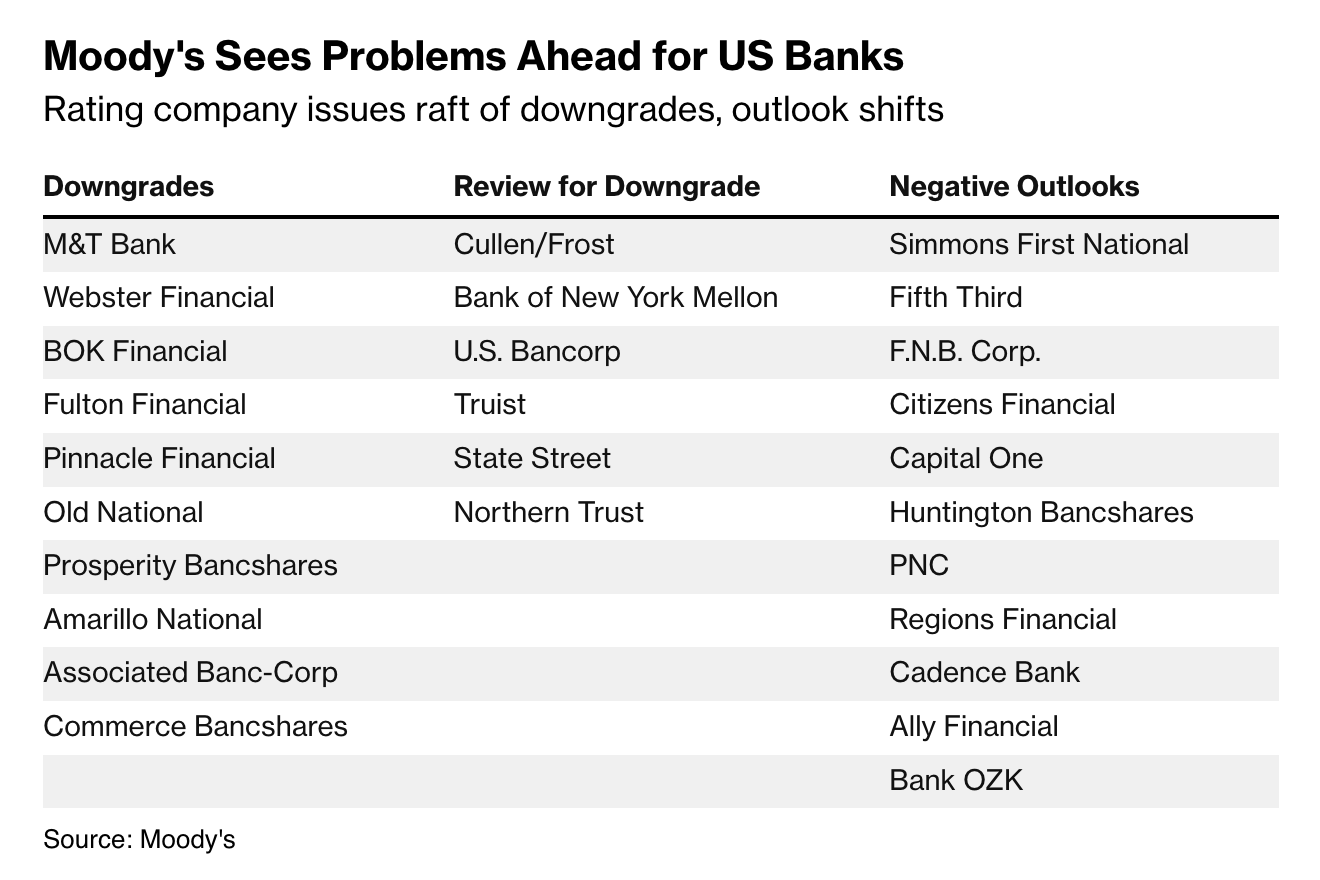

Moody’s just downgraded the credit rating of 10 community and regional banks in early August after a string of other downgrades this year, citing the very thing I remarked as what made them special earlier: their outsized exposure to CRE:

Rapidly rising interest rates caught many banks off-guard and have forced these banks to pay more for deposits and funding from alternative sources. This was a primary driver of the collapses of Silicon Valley Bank, Signature Bank, and First Republic Bank. At the same time, those higher rates have reduced the value of the assets that these banks have on their balance sheets. When there are major declines in the value of certain asset classes, lenders are at risk when loans mature and must be refinanced.

This story, though, doesn’t just start in 2023. There has been a major shift in the industry that requires a look backwards to the Savings and Loan Crisis of the 1980s and 1990s to get some context. Since that time, the total number of FDIC-insured banks has fallen from 14,300 then to 4,500 now including a significant contraction during the Global Financial Crisis:

On top of this, there has been a 14% reduction from 2008 to 2020 in the number of bank branches amongst those banks that remained. This has been driven by the increasing use of technology as well as banks’ desire to protect stock prices by slashing expenses. This is despite the US population increasing from 223 million in 1980 to 340 million today. The effects have been particularly felt in rural, low-income and high-minority areas, according to research by the National Community Reinvestment Coalition. This limits access to debt for critical housing and other community development projects in the very places where high-touch, personal CRE lending services can make the difference between a project getting done and not.

What Developers Are Saying

This year’s banking crisis has coincided with stalling land sales, slowing development, and construction delays across the country. In a great article for the New York Times, Patrick Sisson wrote: "so many housing developments have been sidetracked or delayed that some experts expect a 'production cliff' to hit in a year or so, meaning fewer new homes coming onto the market."

All this is at a time when an unprecedented nationwide housing shortage has progressed to the point where the majority of American renters now spend more than 30% of their incomes simply to make their rent payments. To give you a sense of scale, recent estimates show a nationwide shortage of 7.3 million homes for extremely low-income renters, according to the National Low Income Housing Coalition. We simply cannot afford to stop building, at any scale, in any place, at any time.

The pain from shrinking access to CRE debt is felt most acutely by developers operating at the small to medium scale, as this subset of industry operators is traditionally reliant on smaller, nimbler, and more flexible local banks. Small developers have plenty of financial challenges already (Colette Coleman wrote a brilliant article about this for the New York Times). Their projects often can’t meet traditional risk metrics used by lenders, and that is the consequence of the challenging environments they develop in and the reason for the impact they are hoping to make. Here is a selection of these developers and what they have to say about accessing capital generally, and debt specifically, in their work.

Taylor Bearden, Civico Development - "All real estate is married to finance to a degree and the ways in which we develop projects are shaped in large part by what capital has an appetite for. To put it differently, I think a lot of practitioners of real estate think that they are the origin of what they're doing and why they’re doing it, but the reality is that there is a market that tells them what they can do well before they have the ability to exercise their creativity."

Photo by Erin Clark for Commonplace

Photo by Erin Clark for CommonplaceSonya Rocvil, Bedrock Real Estate Investors - "That puts us in a Catch-22: we haven't done a deal that size before, so it’ll be hard to raise capital for our first one of that size, but also we can’t do one of that size until we’ve raised the capital. And so, one of the biggest barriers we have is just getting people comfortable with our ability to execute on the business strategy."

Photo by Eva Sergeeva for Commonplace

Photo by Eva Sergeeva for CommonplaceMatt Temkin, Greatwater Opportunity Capital – "There's not a robust lending market in Detroit. For a healthy real estate development market, there needs to be more local banks. Many lenders would rather not risk having to take over an asset here. So stabilized financing is not an issue, but acquisition financing or construction financing — those things are tough."

Photo by Nick Hagen for Commonplace

Photo by Nick Hagen for CommonplaceDerrick Tillman, Bridging the Gap Development - "Most projects have requirements around having enough liquidity to serve as a backstop to the project; and, you know, if that was already a struggle in pre-development, there clearly isn't enough liquidity to meet those demands. And also there are guarantees – construction completion guarantees, operating deficit guarantees – which again point back to your liquidity and net worth. To bring it back to us, our net worth is pretty good, but the liquidity is challenging because we have to put the money that we make on our deals and reinvest it into the next project."

Photo by Nancy Andrews for Commonplace

Photo by Nancy Andrews for CommonplaceVictor Baker, Mid-Atlantic – "With the cost of capital and interest rates still increasing, I hear over and over again how pro formas are getting blown up. So if you’re relying on debt, it’s a tough road ahead. If you’re able to balance that with equity, then that writes down the need for debt and allows you to continue securing assets and cash flow. There are definitely opportunities ahead for he or she who has capital. And if not, then I think you’re going to be stuck playing on a smaller level in real estate."

Photo by Eva Sergeeva for Commonplace

Photo by Eva Sergeeva for CommonplaceCoby Lefkowitz, Backyard – "On the debt side, we’ve only used private credit so far because the products that we were building initially don’t have any Fannie or Freddie loans able to support them. We're also in a weird range where we're less than $1 million dollars in construction costs, which is the threshold that a lot of lenders look for in construction loans. It’s just a balancing act of trying to build things that address our housing crisis in an enlightened way, while also rewarding our investors. It is ironic though because we essentially pay banks’ competitors twice as much as we would pay them in interest, and yet the numbers still work and we're successfully refinancing afterwards."

Photo by Eva Sergeeva for Commonplace

Photo by Eva Sergeeva for Commonplace

Outlook

Over the next 2 years, $1 trillion of commercial real estate debt is coming due, which means there will be a massive need for debt for refinancing alone—and it’s unclear who will provide it. For example, the Chief Credit Officer at a local bank in New Jersey remarked to us: "If we don’t know you already, we aren’t lending." This encapsulates what may be the reality: fewer community and regional banks at this size active in the riskiest sectors of CRE, namely office, retail and anything related to construction. That could lead to a number of knock-on effects:

Some smaller banks collapse - Some community and regional banks may not be able to transition to higher yielding debt due to overly conservative underwriting practices that may be based on fear rather than prudent go-forward financial management. Given the higher interest rate environment, this is a lost opportunity to generate revenue. Meanwhile, they have to keep lower-yielding but increasingly-risky, vintage debt for office and retail that is a ticking time bomb. Piskorski estimates that another 186 banks are at risk of default from these interest rate issues alone.

Some smaller banks survive and thrive - Other community and regional banks with more practical underwriting practices, like California-based East West Bank, may increase in exposure. East West Bank is a Minority Depository Institution (MDI), a special type of community and regional bank that focuses on minorities, immigrants, and underserved racial groups while offering loan services to all. Janny Cheung, who is responsible for the eastern region for CRE lending at the bank, said: "We are very prudent in underwriting, balance sheet management and diversification, which leads to stability. We are not a high-leverage lender lender and we want certain deposit requirements."

Wall Street banks move down to smaller deals - The largest Wall Street banks may continue investing resources and improve processes to cater to smaller commercial customer segments, as Wells Fargo has done through the Diverse Segments initiative. The effectiveness of these efforts will be tied to large banks’ abilities to reconsider traditional risk metrics.

More non-bank lenders enter this market - They are often constrained by fewer regulations than banks and are poised to take advantage of capital markets volatility in a big way. An example is ACRE Management, a real estate private equity fund which closed on a $330M dedicated real estate credit vehicle in 2021.

Recommendations for Developers

Now, there is no easy path from here. Ironically, though, that is something with which small to midsize developers are familiar, particularly those with a focus on making an impact. That is due to the many structural problems in the real estate capital markets that the developers featured earlier discussed. These predate the current banking crisis and require incremental innovation and creativity on the part of lenders for change to happen. Going forward, developers should consider the following when looking for debt for their projects:

Know your bank lender - Understand their mission and their track record. More nitty-gritty details like asset diversification, capital ratio, return on assets, return on equity and of course profitability can be discovered through public filings for traded companies. Ask about the exposure the bank has to risky assets and what they do when loans become non-performing. These details paint a picture of how the bank operates and its exposure to risk. More market volatility could lead to the collapse of more banks and having your lender go under is something that you just don’t need in the development process. And to be frank, given the intense scrutiny that small to midsize developers already go through, this type of due diligence of banks may only be fair.

Think before committing - This year’s bank collapses resulted in a flight of capital to Wall Street banks. A partner at a regional multifamily investment fund remarked to us that her LPs refused to wire money for her fund’s latest capital call unless the account was at a Wall Street bank. It is important to remember the value proposition for community and regional banks: they provide high-touch, personal customer service and quick decision making. Also, they can be flexible and responsive to CRE borrowers in special situations, in ways the largest banks may not be able to because of their size.

Learn about non-bank lenders - These capital sources are often at lower cost or operate with a faster turnaround time than their bank rivals. They include the life insurance companies, private lenders, CDFIs, government agencies and government sponsored entities mentioned earlier. They could be poised to grow their books of business as bank lenders contract, if the past economic crises presage what is to come.

Research economic development incentives - Tax credits, tax abatements, grants, and rebates are a key part of diversifying capital stacks to supplement debt and equity. Federal tax credits like Low Income Housing Tax Credits, New Market Tax Credits and Historic Tax Credits can be syndicated and sold to investors to raise construction capital. Other incentives reduce construction costs, reduce operating costs or increase operating revenues. Unfortunately, these are highly technical and often require intense and onerous applications and compliance processes. There is frankly no good solution to make sense of it but tax credit consultants like Heritage Consulting Partners and syndicators like Clocktower Tax Credits can be great resources for small to midsize developers.

Conclusion

The banking sector—which has evolved from the Savings and Loan Crisis to the Global Financial Crisis to now—is intrinsically tied to property-based CRE financing. The banking crisis of 2023 highlighted the outsized role that community and regional banks play in providing debt for the real estate industry in the United States. Banking industry instability, inflation, record high interest rates, a generational shift in workforce habits and a housing affordability crisis are creating problems and opportunities for transforming access to capital for developers looking to make an impact at the small to medium scale. Meanwhile, for the months ahead, a rewrite of the classic Biggie rap anthem may be apt: "less money, mo problems".

— Atif Qadir

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them

Share this post with a friend

Since you liked this post, why not share it to help spread the word?

| A guest post by

|

Start Writing

Start Writing