On Yglesias on Manufactured Homes

A few weeks ago, Matt Yglesias wrote "How to Unleash a Trailer Home Boom," which outlines a strategy for getting more manufactured homes built. Broadly, Yglesias proposes ending HUD code requirements that manufactured homes have a steel chassis, making it easier and less expensive to finance a manufactured home, and removing restrictive zoning practices that prevent manufactured homes in many jurisdictions.

I’m sympathetic to these ideas. Manufactured homes are one of the few ways to reliably reduce the cost of home construction. In 2022, manufactured homes had an average cost per square foot of around $88, compared to $168 for a site-built home.1 Despite this cost advantage, we don’t build that many manufactured homes. In 2022, just 112,000 new manufactured homes were shipped, less than 10% of the 1.5 million housing starts that year. All else being equal, I would like to see more manufactured homes be sold.

Unfortunately, Yglesias’ post seems to rely on incorrect research, and I’m skeptical that the strategy he outlines would actually work to deliver a boom in manufactured home construction.

The HUD code theory of manufactured home decline

Yglesias starts by outlining what I’ve previously called "the HUD code theory of manufactured home decline," which he bases on a paper by Minneapolis Fed economist James Schmitz. According to Schmitz, the passage of the HUD code in 1974 (and more specifically, its requirement that manufactured homes have a steel chassis), was responsible for the collapse of the manufactured home industry, which was poised to take over the single-family home market. Here’s Yglesias:

…as of 1973, the Commerce Department was expecting manufactured housing shipments to continue to rise on the simple logic that productivity was rising in factories but not really on constructive sites. This did not happen, largely because of the National Manufactured Housing Construction and Safety Standards Act of 1974 and the HUD Code that resulted from it.

As James Schmitz of the Minneapolis Fed emphasizes, this law was framed at the time as trying to facilitate the expansion of factory-built housing. The claim was that national preemption of the patchwork of local building codes would make it easier for factories to churn out units. The problem was two-fold:

In practice, the 1960s manufactured home boom was happening in small towns.

Rural areas, at the time, didn’t generally have building codes or land use rules.

So while there was some preemption, in a practical sense a stricter code was being imposed. But here’s the real killer — the code explicitly prohibits homes from being transported on a chassis and then placed on a standard chassis-less foundation.

…Mechanically, the chassis requirement adds costs. Even worse, from a banking standpoint, it means that financing a small manufactured house is more like getting a car loan than getting a mortgage. The chassis is also a target for exclusionary zoning. Towns can (and do) make rules against chassis-mounted homes (or against placing them in certain areas), knowing there’s a federal rule against removing the chassis. So instead of spending the 1980s and 1990s watching small manufactured single-family homes become an increasingly significant player in the non-apartment market, we strangled them.

Schmitz’ paper, however, makes numerous errors, and there’s little reason to believe the HUD code theory of manufactured home decline. I detail this more thoroughly in my post The Rise and Fall of the Manufactured Home, Part II, but here’s a brief rundown of the major errors:

Schmitz argues that the HUD code created new, more stringent regulations where previously there were none. But in fact, nearly every state had manufactured home standards at the time.2 Most standards were based on ANSI standard A119.1, the same standard on which the HUD code is based. Schmitz also fails to mention that pre-HUD code homes had an incredibly high risk of fire, which the HUD code largely solved.

Manufactured homes got cheaper in comparison to site-built homes after the HUD code was passed, not more expensive. Dealers’ own estimates suggest that added costs from the HUD code were very minor.

The HUD code wasn’t a vehicle for manufactured home discrimination. Instead, it made manufactured homes more acceptable to jurisdictions, and zoning restrictions against manufactured homes were reduced after the HUD code was passed.

Schmitz’ idea that the HUD-mandated steel chassis makes it possible for jurisdictions to discriminate against manufactured homes is off the mark. It’s the fact that manufactured homes are built to a different set of code requirements (the HUD code instead of local building codes) that makes it possible to treat them differently. After all, jurisdictions had no trouble discriminating against them before the HUD code and its steel chassis requirement was created. Removing the steel chassis requirement would reduce costs (and I’m for it for that reason), but jurisdictions could still discriminate against them based on the different code of requirements. Physical distinctions are not prerequisites for discrimination–physically indistinguishable things can be, and are, treated completely differently by the government based on the paperwork attached to them all the time. For example, non-citizens are treated differently than citizens.

While removal of the steel chassis requirement in the HUD code would be a positive development, there’s no real reason to think that it's doing a lot of work to prevent manufactured home placement. Schmitz’s paper contains basic errors and people should stop citing it.

Manufactured homes as real estate

The next leg of Yglesias’ strategy is to improve manufactured home financing. Manufactured homes are often treated by the state as personal property, rather than real estate. This means that manufactured homes are often financed with high-interest "chattel" loans instead of lower-interest mortgages available for real estate. Per Yglesias, if states made it possible to treat manufactured homes as real estate, rather than personal property, financing them would be easier, and more of them would be built.

There’s a few issues with this idea. For one, many states make it possible for a manufactured home to be real estate, rather than personal property. Fannie Mae gives an exhaustive, state-by-state list of the procedures for doing this. Typically it requires filling out some paperwork, and permanently attaching the manufactured home to the site. Only five states – Connecticut, Hawaii, Massachusetts, New York, and Rhode Island, along with Washington DC – have no procedures for doing this (and even some of these states will in practice treat manufactured homes as real estate in some cases).

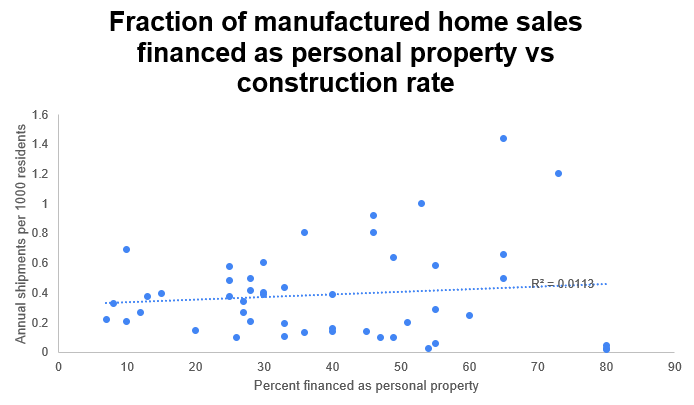

Similarly, financing manufactured homes with mortgages is very common. A 2019 study by the Consumer Financial Protection Bureau found that when you include sales of used manufactured homes, chattel loans make up just 42% of loans for manufactured homes, with most of the other 58% financed by lower-interest mortgages. And this varies significantly by state. In some states, like Washington, nearly all manufactured home sales are financed with mortgages.

Moreover, there doesn’t seem to be much of a relationship between how often manufactured home purchases are financed with mortgages, and the rate of manufactured home construction. States with lots of mortgages don’t build more manufactured homes than states with lots of chattel lending. If anything, the relationship is in the other direction.

It does seem like there’s room for improvement in manufactured home financing. Most new manufactured homes are financed with chattel loans, and a 2018 study by the Urban institute found that many buyers who got a chattel loan were eligible for a lower-interest mortgage. But with manufactured home mortgages so widely available, it’s not obvious to me what specific improvements would help here.

Manufactured homes and zoning restrictions

The last part of Yglesias’ strategy is to reduce zoning restrictions that prevent or limit the placement of manufactured homes.

It’s true that many jurisdictions use zoning rules to try to prevent manufactured homes from being placed (this Reason piece gives several examples, and the Manufactured Housing Institute lists several more). It seems reasonable that reducing zoning restrictions would go a long way to increasing manufactured home sales. However, it’s hard to know what zoning changes are most important: many attempts at doing this don’t seem to have worked.

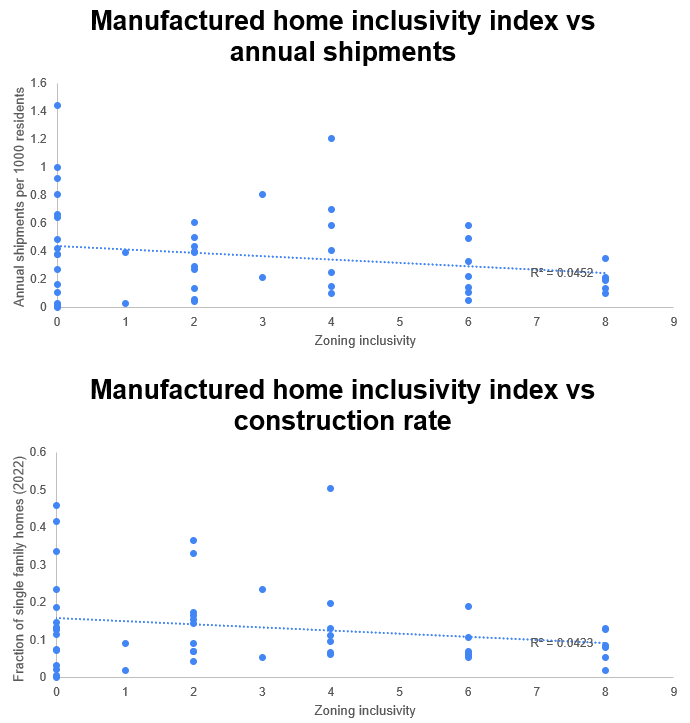

For instance, the 2011 HUD paper "Regulatory Barriers to Manufactured Housing Placement" created a "regulatory inclusion index" to measure how permissive different states were towards manufactured home construction. States scored higher on the index by treating manufactured homes as real property, by requiring local jurisdictions to allow manufactured homes, and by not having specific design standards for manufactured homes. The higher a state's index score, the more permissive it was towards manufactured home construction.

However, if we compare these index scores to actual rates of manufactured home construction (either in per-capita terms or as a fraction of overall home construction), we see almost no relationship. The more permissive states don’t build more manufactured homes than the less permissive states (once again, if anything the relationship goes in the opposite direction).

You can of course argue that this index isn’t an accurate measure of manufactured home zoning restrictions, but this is exactly my point: it's hard to know which restrictions matter most. These are the ones that HUD thought were important, and if anyone would know it seems like HUD would. But apparently they were wrong.

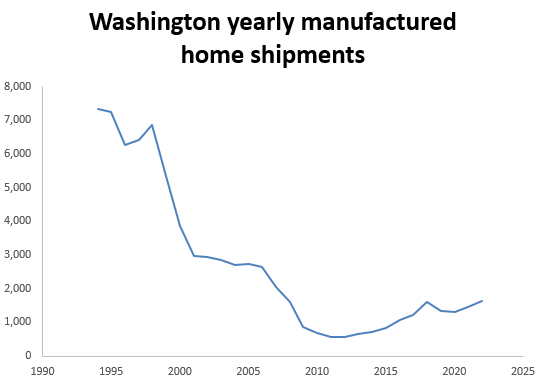

We see something similar if we look at state-level trends. Washington, for instance, passed a series of laws in the 2000s to encourage manufactured home construction. Most importantly, in 2004, it required local jurisdictions to regulate manufactured homes similarly to site-built homes. However, this didn’t have any noticeable effect on the number of manufactured home shipments in Washington.

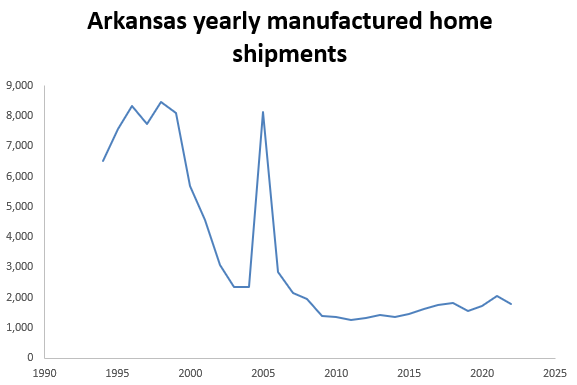

Likewise, Arkansas in 2003 passed the "Affordable Housing Accessibility Act," which requires jurisdictions to allow manufactured homes in at least one district, and disallows restricting them only to trailer parks. But like in Washington, there was no noticeable effect on the long-term trends in manufactured home shipments (though there was a large spike in 2005, it’s unclear if that's real or a data artifact. Regardless, it reverted the following year).

These are both notably different from the California ADU law, which almost immediately resulted in an increase in the number of ADUs built in the state.

There’s some evidence of impacts in the other direction: cases where adding more restrictions results in a drop in manufactured home shipments. In Georgia, a 1990 state Supreme Court ruling determined that jurisdictions couldn’t ban manufactured homes from all residential districts. In 2003, the state Supreme Court reversed that decision, allowing jurisdictions to ban manufactured homes from all residential districts if they so desired. The 2003 ruling did coincide with a substantial drop in manufactured home shipments. However, this drop occurred in the middle of a long-term decline in manufactured home shipments, which was also seen in many other states like Arkansas and Washington, so it's hard to tell what effect this actually had.

California is another illustration of the difficulty of improving manufactured home construction. California has some of the most permissive manufactured home zoning laws in the country (the director of the California Manufactured Housing Institute has gone so far as to say that California "has no zoning problem"). But in 2022 California’s rate of manufactured home building was just half the national average: less than 4% of housing starts in California were manufactured homes, compared to around 7.5% nationally.

So while many states have zoning restrictions that limit manufactured home placement, it's far from obvious what changes would actually make a difference here.

Conclusion

I'm in favor of building more housing, and taking greater advantage of manufactured homes. But to get them we need interventions that will work, and it's hard to know what those are. This would be a good project for an academic interested in housing issues to study: what interventions would increase the number of manufactured homes shipped?

Thanks to Aidan Mackenzie for doing much of the research on this post.

This isn’t quite comparing apples to apples, but we still see substantial cost savings if we compare homes with similar features. See here.

At the time called mobile homes.

Subscribe to Construction Physics

By Brian Potter · Hundreds of paid subscribers

Why buildings are built the way they are.