Another Day in Katerradise

constructionphysics.substack.com · by Brian Potter

Last week the construction startup Katerra declared that it was shuttering it’s US operations, putting another L on the board for Softbank’s Vision Fund. It is walking away from numerous in-progress construction projects, its employees are being let go, and its assets are being sold.

The immediate cause of Katerra’s bankruptcy seems to be the bankruptcy of Greensill Capital, another Softbank-backed startup. At the beginning of 2021, under severe financial strain, Katerra underwent a recapitalization that cut its valuation by 90% (from $4 billion down to $400 million). As part of this, Katerra negotiated away a $440 million debt owed to Greensill, a supply chain finance company. But a few months later, Greensill itself went bankrupt, and the owners of this debt (Credit Suisse) are claiming that Katerra still owes it, which is apparently preventing the company from getting construction bonding. Since the debt is more than the current value of the company, that obviously presents a challenge.

Despite the scale of Katerra (it raised over $2 billion in venture capital, had offices in 9 countries, and employed over 8000 people at its peak), very little information about the company’s internal operations was ever public, and it got comparatively little press attention. Most of the takes and analyses diagnosing Katerra’s problems aren’t particularly well-informed - none, for instance, even get Katerra’s basic business model correct.

I worked at Katerra for 2.5 years, from early 2018 to the end of 2020, and had a first-hand look at how a company that seemed so promising ended up where it did. Since no one has yet written anything that really captures what it was like there, or what Katerra was trying to do, I figured I would try.

The Beginning

Katerra was originally founded in 2015 by Michael Marks, the former CEO of Flex, a contract electronics manufacturer. Marks grew Flex (then Flextronics) into the largest contract electronics manufacturer in the world [0], growing it’s revenue from under $100 million to over $14 billion during his tenure.

The origin story of Katerra was that Marks was at lunch with a real estate developer, who pointed out a couple of his projects under construction nearby. Marks made a comment to the effect of "you must be getting a great deal on your toilets, since with two projects you're buying so many of them". The developer explained that that wasn't how construction worked - the projects were with different architects, different contractors, and there weren't really bulk purchasing discounts.

The story itself is probably apocryphal, but that's the opportunity Katerra was originally founded to address. Success in electronics manufacturing requires a ruthlessly efficient supply chain, and Katerra was originally founded as a supply chain and logistics company. The company would source building materials inexpensively and in bulk from China and other places.

As the story goes, this business model didn’t really work - architects and designers weren’t willing to specify Katerra’s products, they wanted to use what they were familiar with. So early on Katerra pivoted to become a completely vertically integrated construction company. They would still source their own materials, but use them in Katerra designed and built buildings [1].

Compared to the electronics manufacturing world, I’m sure the construction world looked astonishingly primitive, and modernizing it became another key part of Katerra’s value proposition. Instead of laboriously constructing buildings one at a time, by hand, buildings would be built the way everything else was built - prefabricated in a factory, designed specifically to be manufactured as efficiently as possible. Instead of designing buildings from scratch every single time, Katerra would have building products: standard, off the shelf buildings that could be customized for a client’s needs, the same way mass produced cars offer a wide variety of trim options.

This was the Katerra playbook when I joined the company. They would design a series of building products that could be mass-produced in their own factories, leveraging economies of scale and advanced manufacturing to build more efficiently than conventional construction. These products would be full of Katerra-supplied materials - everything from lightbulbs, to countertops, to bathroom fixtures, to appliances would all be Katerra brand. They would acquire general contractors in different markets to give them a nationwide construction footprint, and hire the various trades to self-perform all the construction work. At the time, I thought this was the exact right strategy needed to change the construction industry - it couldn’t be done piecemeal, it needed to be done all at once, simultaneously attacking every stage in the process.

Scaling Up

I joined Katerra early 2018; my role was to help grow and manage the Atlanta structural engineering team, which would be part of an Atlanta-based team of architects and engineers. By then Katerra was already a large company - I was somewhere around employee number 1000, and in North America alone Katerra already had offices in Menlo, San Francisco, Seattle, Vancouver, Spokane, and Phoenix. Worldwide, they had locations in India, UAE, Dubai, and China. They had already built factories in Phoenix and Spokane, and had more planned for California, Texas, and the southeast.

In those days, Katerra’s goal was scaling up as fast as possible. In less than a year the Atlanta structural engineering team went from 3 to 11 people. Katerra was an ambitious company tackling the biggest problems in the construction industry, and that helped us recruit extremely talented and motivated people. People point to Katerra as an example of the mis-steps by non-industry veterans, but we actually had an incredibly easy time recruiting extremely knowledgeable, experienced industry folks who were sold on the vision - the entire structural department (40+ people spread across 5 offices) ended up being a real murderer's row of talent [2].

It was an exciting time in the company - I joined just a few days after Katerra had secured $865 million in financing from Softbank, and there seemed to be unlimited opportunity ahead of us. After a few months in various WeWorks, we moved into the extremely plush offices of an architect Katerra had acquired (temporary quarters until the buildout of an entire floor to contain the future 150+ person team was complete). We joked that our marketing materials were constantly out of date, as by the time they were printed we had hired more people and opened more offices. In that year Katerra would octuple in size, growing to over 8000 employees.

Katerra’s Building Systems

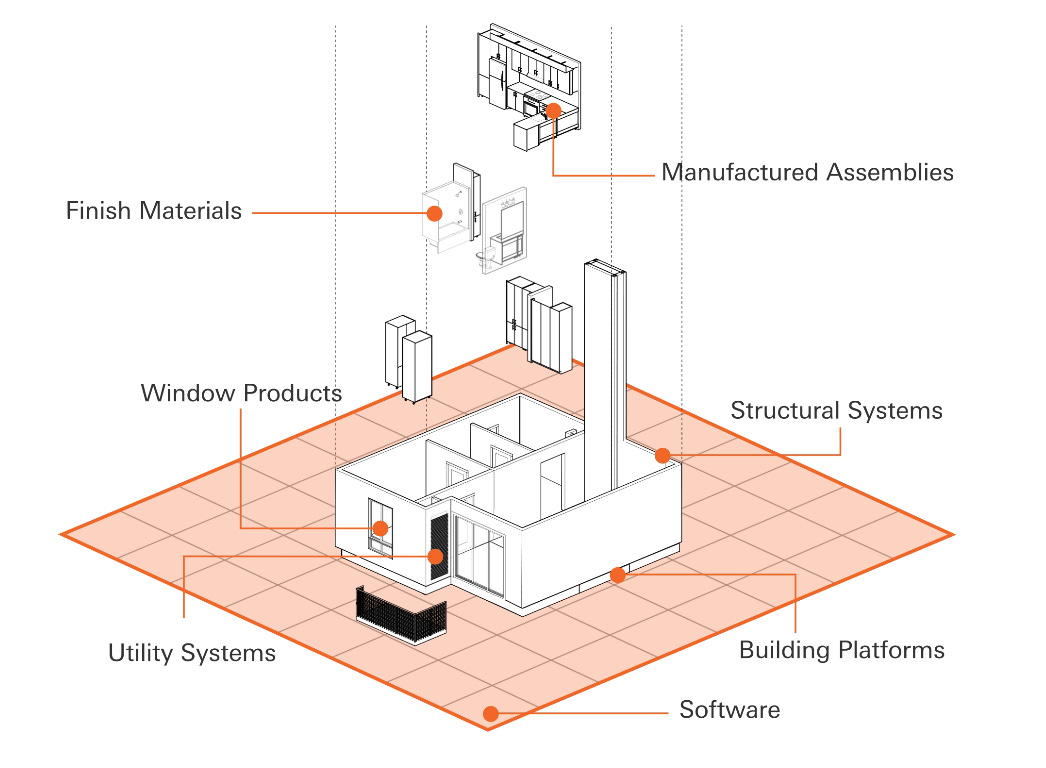

Katerra had ambitions to eventually construct buildings of all types, but it initially pursued the multifamily residential market. Its buildings were based on light framed, panelized wood construction - Katerra’s factories would produce prefabricated wall panels and floor cassettes (floor trusses joined by sheathing into a single floor panel). This is a fairly common building system, but Katerra hoped to differentiate themselves by using panels with a higher level of completion: Katerra panels would have windows, plumbing stacks, and electrical boxes all pre-installed in the factory. The goal was to eventually produce fully enclosed, high level of completion panels that would contain all the required building systems (including drywall and exterior finishes), and could be erected on site with almost no field work required. It was an ambitious goal - I’m not aware of anyone in the industry doing it at scale.

We’ve covered the difficulties of making a factory-built housing system profitable ad-nauseum. But Katerra’s business model actually gave them a lot more leeway to make the model work. They could (theoretically) afford to sell buildings for at or near cost, and simply use them as a vehicle to sell as many building materials as possible (similar to how manufactured home builders often make a large fraction of their profits from financing the homes). But the economics of factory production still hold - making the numbers work requires maximizing your factory’s production volume. Katerra planned to do this with a series of standard, off-the-shelf buildings that it could prefabricate and sell all over the country.

Katerra Products

Katerra’s products were what would differentiate them from conventional construction, as well as from more "traditional" modular construction. The company saw a huge opportunity in the fact that conventional construction was dominated by custom, one-off designs, and invested heavily in the idea of productizing entire buildings - off-the-shelf building designs that had been designed for maximum fabrication efficiency, and could be built better, faster and cheaper than anything conventional construction could match. In retrospect, the way this was executed seems like another page out of the electronics manufacturing playbook - Katerra planned on designing products based on customer’s specifications, while also offering their own in-house line of products.

The product development effort simultaneously felt both enormous and chronically understaffed. There were hundreds of people working in product development (though a relatively small fraction of them were actual engineers or designers), and the number of products in development at one time was staggering. In addition to entire buildings, the product development effort included individual building systems and components, as well as construction software. I’ve done my best to compile a full list below:

Buildings

Garden apartments (K3)

Large multifamily apartment building (Corridor)

Workforce housing building (K4)

Midrise mass timber office building (MTOP, later MROP)

High rise residential building

Industrial building with CLT walls

Single family home

Precast home for construction in Saudi Arabia

Construction office product (KROC)

10-story multifamily building for India (K10)

Building Systems

Fast foundation system

CLT panels

Prefab bathroom kit

Prefab kitchen kit

Air conditioning system (KTAC)

Energy storage system (KES)

Katerra windows

Katerra cabinets

Raised office floor made from CLT

Conference room partition system

Low-carbon concrete (K-Crete)

CLT façade system

Software

Apollo, a suite of construction management software

Automated building design software

Tenant management app for use by landlords

And this doesn’t include the materials Katerra was developing and selling. Among these was Katerra’s own brand of appliances and fixtures (KOVA), some of which were rebranded products built by other factories, some of which had been designed internally (such as some lighting products).

These products varied in the amount of attention given to them. Some of them (like the garden apartment) had hundreds of employees, millions of dollars in development budget, and years of design time. But many others lacked the resources required for a serious development effort, and operated with a shoestring budget and a tiny staff.

Ideally, early stage product development involves rapid iteration and prototyping, to figure out what needs to be built as quickly as possible. But the pace of product development at Katerra always felt sluggish. Products would spend months or years in various stages of design without ever so much as a prototype being constructed. (the garden apartment product mentioned above had just begun construction of the first prototype project, after 3+ years of development, when the company shut down).

This was in part due to the difficulty of getting prefabricated construction cost-competitive with site built - designs would get sent to estimating, come back with a cost that was too high, and go back for redesign. Most of the products spent their entire life lingering in the design phase (the ones that I’m aware of making it into actual production were the precast home, the lighting, the bathroom and kitchen kits, and the windows).

CLT

One material Katerra sold that deserves closer examination is CLT. CLT is a mass timber panel product, sort of like a super plywood. CLT panels are made with alternating layers of dimensional lumber, resulting in large panels that can be used as the floors, walls, and roof of a building. CLT is a comparatively new building material - it was developed in Europe in the 90s, but has seen relatively little use in the US.

Katerra bet very heavily on CLT, investing somewhere in the neighborhood of $100 million on a plant for producing it, and for a while it was a defining aspect of the company (I remember brushing up on the PRG-320 guide on the plane ride out to the interview). As part of this, Katerra acquired a lot of high-end mass timber design talent (including the architecture firm MGA and the engineering firm Equilibrium, both of which specialize in mass timber). Emphasizing CLT almost certainly helped out recruiting efforts, at least on the design side - there’s a lot of enthusiasm for the product in the architecture and engineering world.

There’s actually a lot to like about making CLT part of the business model. Since it’s a high-end material, it immediately helps differentiate your product from what people typically imagine when they think of "factory produced housing". It’s factory built and panelized, dovetailing nicely with the rest of Katerra’s prefab building systems. It’s environmentally friendly, and upcoming building code changes make it easier to specify. It seems like a case of skating to where the puck will be - CLT’s rising popularity and limited availability meant Katerra could have been a major producer in an expanding market. For a company whose bread and butter was material sales, it seems like an astute choice.

The problem is that once that decision was made, it was hard to change direction. The Katerra CLT factory could produce something like 10% of the total global supply of CLT, which required selling a LOT of it. This ended up being difficult to do - CLT is an expensive product, and an easy target for value engineering if project costs are too high (we ended up seeing it get cut from a lot of projects). I suspect the recent lumber price increases have only made this issue worse.

Acquisitions

In addition to Katerra’s rapid hiring (dozens and dozens of new hires every week), Katerra also grew through acquisitions. Acquisitions were, broadly, focused on two areas: providing Katerra a nationwide construction footprint (by acquiring contractors such as Fields, Fortune Johnson, and UEB), and acquiring design capabilities (in addition to Equilibrium and MGA, Katerra also acquired several other architects in the US and abroad). But there were plenty of other acquisitions as well - a lighting supplier, a concrete contractor, and a software company to name a few. One of the largest deals was a merger with KEF Infra, a massive precast concrete company in India.

Most of these companies continued to operate similarly to the way they did pre-acquisition. The design companies continued to bid for work, the contractors continued to build outside projects, etc. This gave the company a large number of revenue streams, but it also meant Katerra often had trouble operating as a single, unified whole [3]. Theoretically, all the different divisions could have been each other's clients - engineers, architects, contractors and trades all working together on the same projects. But in practice this proved difficult - most of these groups already had folks they were comfortable working with, and it probably seemed needlessly risky to switch to working with a team they had no experience with, whether they were part of the same company or not.

There never ended up being systems in place to facilitate different business units working together - it remained difficult throughout my time at the company. So for instance, the engineering team almost never worked with the renovations department, despite having several engineers very experienced with renovation work.

This meant that any initiative that crossed business unit lines ended up being a constant source of headaches and frustration. An example: a change on an active project that would have resulted in a million dollar savings took months of internal negotiation to push forward, because it would have changed the scope of work for the engineering team. This sort of local optimization was rampant, and often left a lot of potential improvements on the table. The fact that nearly every division was expected to be a profit center probably exacerbated this. For instance, we asked for months for a way to track time that would allow us to assist an acquired architect (that we were sharing an office with) on early stage project work. We were ultimately told not to do this, and spend our time on billable things.

Bureaucracy

In some ways Katerra had the worst aspects of both a young, nimble startup, and a large, entrenched bureaucracy. The rapid growth meant that everything was constantly in flux (reporting structures, department goals, even office locations), but the sheer size of the company meant that things were extremely difficult to change deliberately. Each new acquisition and hire added more stakeholders, and changed the way that decisions got made.

Every company inevitably develops informal channels and processes of how things are accomplished - who has the knowledge about a particular initiative, who can be pushed on to loosen a potential blockage, who you have to follow up with, who not to engage, etc. With the constant acquisitions and scaling up, and the lack of deliberate integration of acquired businesses units, this landscape was constantly shifting, making it hard to keep things moving forward.

I suspect this is part of the reason for the slow pace for product development. New people would come in as a result of acquisitions, or get shifted around, and the product direction would change. It took a huge effort to just maintain forward progress, simply due to the entropy of the company structure. The amount of people required to sign off on a change kept going up, and as the company grew each approval got harder to receive, as demands on the approvers time went up. Things that could have been tested in a single weekend by a small, scrappy company would drag on for months at a time.

For instance, one of the necessary parts of the building product development was creating a software workflow that could translate Revit data into a set of instructions read by the factory equipment. The number of stakeholders involved meant there was no good way of rapidly experimenting to figure out the best method and implement it. As a result, months of effort would get spent trying to get a particular solution to work.

Product Market Fit

Anyone looking for them can find plenty of horror stories about Katerra - projects that were delayed and over budget, mistakes that were made when setting up the factories, outrageous levels of spending, etc. But every large company, especially one that is rapidly growing, has horror stories. Katerra spent money like it was going out of style (at one point they had two company jets leased), but so did plenty of successful startups. Katerra had an incredibly frustrating bureaucracy, but all large companies have incredibly frustrating bureaucracies. Katerra had some projects go sideways, but every construction company has projects go sideways. Anecdotal descriptions of problems don’t provide much information, because we’d expect a lot of problems whether or not Katerra was succeeding. We need to look a bit deeper to diagnose the structural issues with the company.

Ultimately I think Katerra’s struggles can be traced to a lack of product-market fit. The company scaled up massively prior to having a product people wanted to buy, and it spent several fitful years (and painful pivots) trying to find one. Katerra started out heavily CLT focused, shifted more towards light framed wood, took a quick detour to cold formed steel, then went back to wood. An entire division was hired to self-perform construction work, then later eliminated. The engineering department was tasked with selling outside consulting services, then cut by 75% after we had lined up a backlog of work.

Each change stretched out timelines, and consumed massive amounts of resources in capital expenditures and design budgets. The pivot to cold formed steel, for instance, resulted in purchasing incredibly expensive CFS roll formers, acquiring CFS fabricators, hiring for CFS expertise, and completely redesigning several products.

In some ways, this is a boring answer - the most likely thing to kill a startup, killed a startup. A pivot is hard enough at a small startup. It’s far harder at one that employs thousands of people, and has massive capital investments in building physical products.

What Goes Up...

The first year and a half at Katerra was incredibly rewarding. Many of us worked incredibly long hours out of sheer enthusiasm and excitement. But as time went on the cracks began to show.

Reorganizations continued to happen (in my first year, the engineering department was moved 3 times). Relatively straightforward management issues (like getting title bumps pushed through) somehow became impossible obstacles. Most worryingly, the flow of new projects slowed to a trickle. Products kept getting priced and coming back too expensive, or would go on hold and not come off. New projects failed to materialize.

The turning point (for me at least) was the end of Summer 2019. There was a massive series of layoffs that cut our group by 75%, and essentially obliterated everything we’d been working on and planned to accomplish.

Everything after that feels like sort of a rearguard action. Shortly after there would be a new CEO installed, and the company became laser focused on (sorely needed) cost reduction. The year that followed was a long, brutal series of layoffs (when I left in October of 2020, I had survived 5 or 6 rounds of layoffs, and there were more after I left). Perks and benefits were cut, the Phoenix factory was closed, R&D got slashed to the bone, and most product development efforts outside of a few critical ones were cancelled. Self perform was eliminated as well.

But the problems of scale continue to apply even when you try to de-scale. The lack of structure meant that management didn’t have good visibility on who needed to be let go and who should stay, and we frequently found that critical colleagues had been let go, leaving groups without the right resources or staff. Simply maintaining existing commitments became a herculean effort. I ended up leaving in October of 2020, prior to the recapitalization that cut the company’s valuation by 90% and wiped out existing shareholders).

It should be said that there’s likely a bit of narrative fallacy here - Katerra had some struggles but also a lot of bad luck: the WeWork blowup (which precipitated the focus on cost-cutting), the pandemic, the lumber price increase, the Greensill bankruptcy, . It's easy to imagine that if one or two catastrophic things hadn’t happened, Katerra could have made it through, and become an amazing story of company survival. Anecdotally, up until the announcement they were closing last week, folks at the company seemed fairly pleased with the trajectory it was on.

Katerra was, in the words of Paul Graham, frighteningly ambitious. It planned on offering products that could cover 80% of the built environment (apartments, houses, hotels, office buildings, industrial buildings, and plenty more), and recruited an army of people who tried their absolute best to make it happen. You’ll find a huge number of ex employees that loved their time at Katerra, and consider it some of the most valuable and meaningful work they ever did. One anecdote for the extent that folks were bought in - during the call announcing the recapitalization (that wiped out existing stockholders) someone asked if employees would have the option to buy back into the company into the future). My LinkedIn has been completely flooded with "end of the road" type announcements, and nearly every one of them is about how much they valued the opportunity they had at Katerra.

Katerra didn’t end up working, but I’m glad we had the opportunity to try.

[0] - Today it’s a distant third.

[1] - This probably explains why Katerra didn't end up taking on the property developer role, and instead tried to work with other developers. Doing property development (which requires huge investments in land, and lots of local real estate knowledge) is sort of orthogonal to the business of trying to sell as much material as possible.

[2] - One example: one day an engineer mentioned he’d be out for an hour during the day, because he was being interviewed by Engineering News Record about a previous project of his that had won Project of the Year.

[3] - One interesting side effect of this is that a lot of these companies have been able to relatively quickly extricate themselves from Katerra and continue their operations.

Feel free to contact me!

email: [email protected]