Net Lease Real Estate

Pairing bond-like income with real estate upside, net lease real estate models are an under-appreciated investment thesis.

Thesis Driven dives deep into emerging themes and real estate operating models. Today’s letter is from guest contributor Jonathan Andrews, a real estate developer and investor with Arch Companies. It digs into net lease real estate models with a focus on the automotive subsector.

Commercial real estate is at an inflection point, undergoing one of the largest shifts in the way we occupy the built environment in the past 50 years. In the face of today’s changing demands for space and evolving consumer preferences, what real estate sectors are slated to emerge as likely winners in the coming decade? Asking ourselves the "10-Year Question" prompts a very simple two-part query: in ten years, what will the world look like? And what are the asset classes, subsectors, and products which will outperform in that world?

Specifically, certain segments of real estate beyond the "four food groups"of office, industrial, retail, and multifamily have seen a greater preservation of value than others. Key winners in this space are generally included in the broad category of "real estate alternatives" and other specialty asset classes

. Today’s letter will focus on net lease real estate, an oft-overlooked alternative real estate sector.For those not as familiar with the category, net lease offers investors several benefits in today’s inflationary and high interest rate environment. Yet not all net lease is created equal, as the definition includes both victims of the pandemic (such as office buildings and movie theaters) as well as clear winners (such as QSRs and industrial properties). This letter will offer an overview of the net lease category before diving into a lesser-known but strong net lease performer: automotive real estate.

Sector Overview: Net Lease

Typically, "net lease" real estate is shorthand for "single tenant net lease" assets. This refers to a leasing structure in which tenants are responsible for payment of all expenses related to the care of a property (i.e. real estate taxes, insurance and maintenance). It is a popular asset class amongst mom-and-pop investors, which make up the vast majority of the investable net lease universe– as it generally requires a smaller amount of capital to purchase individual properties for passive cash flow. Though this article focuses specifically on retail, "net lease" real estate also includes single-tenant office and industrial assets.

Net lease assets are traditionally seen as a bond arbitrage play. The corporate bond yield of a credit tenant historically sits ~240 bps below the cap rate of a hard asset occupied by a similarly rated company

. This is due to the perception that owning physical real estate is seen as inherently riskier to own over a financial instrument. Yet these leases feature key benefits over bonds, such as built-in rent increases and the potential for appreciating value of the underlying asset, both of which serve as hedges against inflation. Therefore, while a bond only returns at a fixed rate, net lease assets with credit tenants provide "bond-like" performance – backed by corporate guarantees – but have the potential to outperform their actual bond counterparts.The net lease market tends to be quite fragmented and inefficient, with a significant number of smaller investors in net lease retail when compared to other asset classes. Of the roughly ~$12 trillion global investable universe of net lease assets in Europe and the US, only $100 billion is held in by publicly-traded investors. Hence the sector features relatively fragmented ownership, with small owners rather than a select few institutions holding the bulk of net lease assets

. This creates significant market roll-up potential for institutional buyers.One should also factor in the difference in the investment strategies between institutions and individuals and its impact on the sector’s pricing resilience. Besides the fact that non-institutional investors tend to write smaller checks – since they don’t have the capital for large, big-ticket multifamily or office assets – they are also not bound by the same requirements to achieve short term gains by liquidating positions (e.g. as in the case of close-ended funds), or rebalance portfolios (e.g. such as a large LP, who would face those requirements). Instead, investment motivation is often driven by the desire for high yield, passive cash flows, or favorable tax treatment.

For a sector such as retail net lease, this preponderance of small owners contributes to the sector’s general trend resisting radical swings in pricing (as we’ve also seen in other inefficient asset classes, such as mobile homes and self-storage) This is particularly shown in times of pricing volatility, where there is even less impetus to sell in a down market - an excellent example is the reduced transaction volume across net lease over the past two years.

Sector Headwinds and Future Prospects

Despite the clear value proposition of the sector, the current interest rate environment poses serious challenges for the institutional investor. With average retail NNN cap rates hovering around 5.95%, and a current Federal Funds rate around ~5%, bond yields for corporations are now outpacing those of implied cap rates for comparably-rated tenants.

With the historic spread between brick and mortar retail yields and corporate debt now much diminished, how can investors gain access to the sector?Best-in-class net lease owners such as Blue Owl Capital utilize strategies such as sale-leasebacks to achieve much higher going-in yields than what is available on the open market. By originating their own deals and going directly to the sellers themselves, Blue Owl is able to drive better terms with franchisees and owners than what might otherwise be seen on the open market. As a result, investors could expect to achieve a spread ~200-300bps above what a similar deal might trade for when listed by a broker. Indeed, with today’s pressures of high lending costs on corporations, sale-leasebacks provide an attractive financing alternative for those in need of cash – in today’s environment, equity has become the new debt.

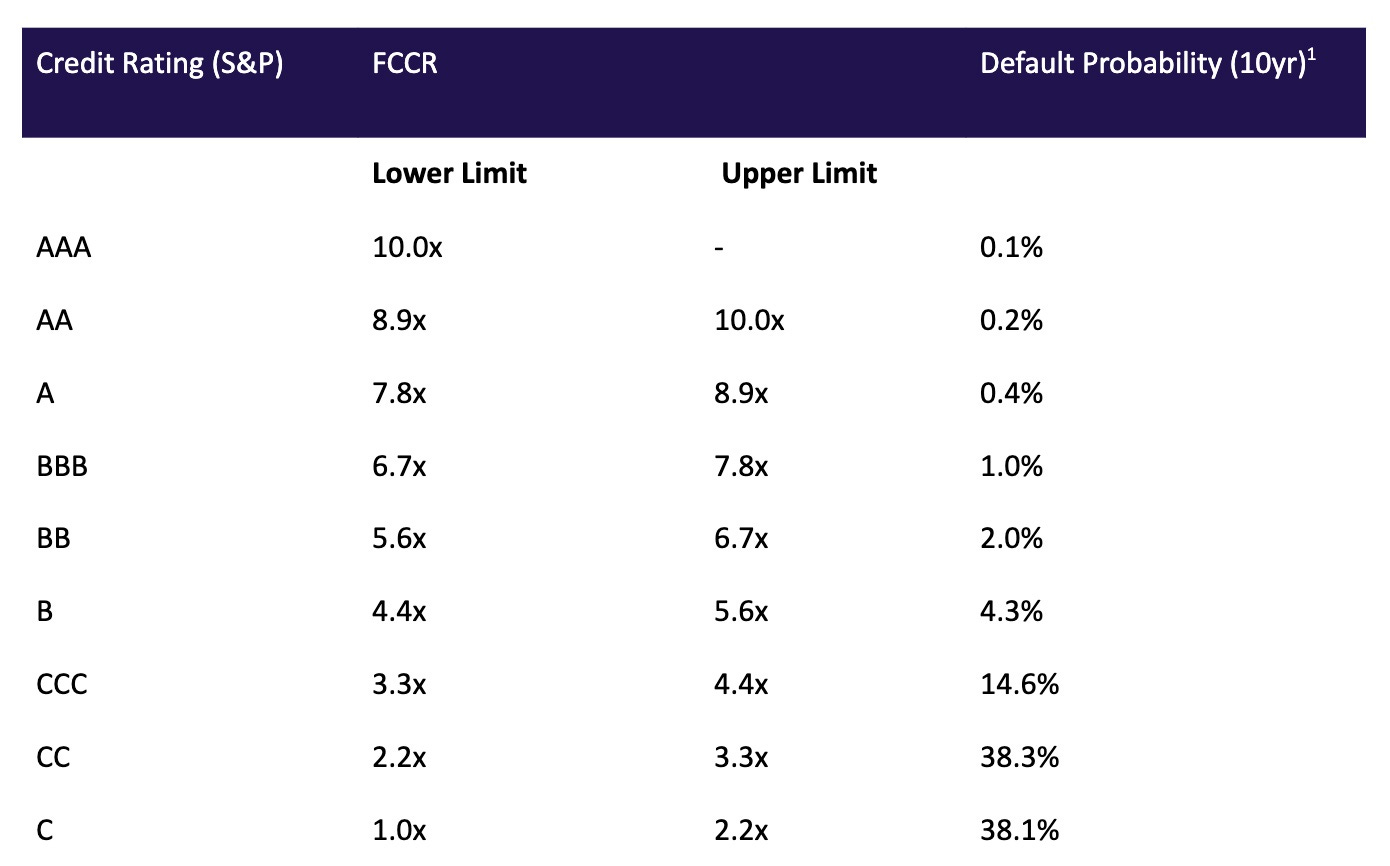

Another strategy to achieve greater yield is to focus on underwriting non-credit tenants as potential investment targets. REITs such as STORE Capital have refined this practice, applying alternative valuation metrics based on rent coverage ratios compared to net revenues. By measuring asset performance at the unit level, rather than intuiting the likelihood of rent payment and renewals according to credit rating, an investor can utilize a different metric for making appropriate valuations when acquiring properties. To give an example of how this could work, an asset occupied by an established non-credit tenant might trade in the 8% cap rate range. However, the store itself might also feature a high "fixed cost coverage ratio" (or FCCR) of 6.0x (based on their EBITDA).

FCCR is a ratio commonly utilized in the world of corporate finance, and plays a useful role in this analysis. It compares the cost of fixed expenses a business incurs, such as debt service or lease expense, as a ratio to its overall earnings before interest, taxes, depreciation, and amortization (or EBITDA). Assuming you can estimate the lending costs a tenant is incurring through reviewing their books, you can arrive at this FCCR figure relatively easily.

EBITDA = earnings before interest, taxes, depreciation, and amortization

FCBT = fixed charges before tax

i = interest

As a thought experiment, let’s now set an evenly-weighted scale of 1.0x to 10.0x FCCR as the bond range between C and AAA, using S&P’s rating system. A 1.0x FCCR would correspond to a ‘C’ credit rating – this would imply that the tenant has just enough money to pay their rent (and hence is very likely to default). Meanwhile, a 10.0x FCCR implies that the tenant has ample cash to cover expenses (and a correspondingly low probability of default) – here we will ascribe a ‘AAA’ rating.

Using this kind of metric, we can see that the implied likelihood of default for this hypothetical tenant with a 6.0x FCCR is relatively low–perhaps equivalent to that of a ~BBB-rated credit tenant (where bonds trade in the ~5.75% range today).

From this perspective, this seemingly "riskier" non-credit investment actually might be dramatically undervalued, and hence a good purchase.While this metric should be adjusted to factor in an average FCCR on an industry-by-industry basis to be more accurate, it provides a rough analytical framework through which investors can concretely think about assigning risk. Going back to the fact that net lease is an asset class based on the underlying fundamentals of the business occupying the space, it follows that understanding the company’s cash flows and performance should always be a critical component in any real estate investor’s underwriting.

Whereas average net lease cap rates on the market currently hover around 6.0%, strategies such as originating off-market deals through sale-leasebacks, (or otherwise leaning on alternative underwriting standards when determining value) can lead to better returns. Assuming appropriate entry cap rates in the ~8.0% range,even moderate leverage in today’s environment can lead to cash-on-cash yields in the low-double digit range. For those investors who believe that rates will come down again over the next 12-24 months, this moment in time represents a unique buying opportunity. A return to "normalized" cap rates could translate into a significant windfall for those investing in net lease deals today.

So while today’s rising rates are driving down prices and reducing transaction volume in the sector, deals are still getting done. But executing a net lease business plan in the current environment requires that investors actually add value by bringing unique insights and analysis to the table. To paraphrase from Howard Marks, you can’t expect to see investment outperformance with conventional investment strategies.

Subsector Overview: Automotive Net Lease

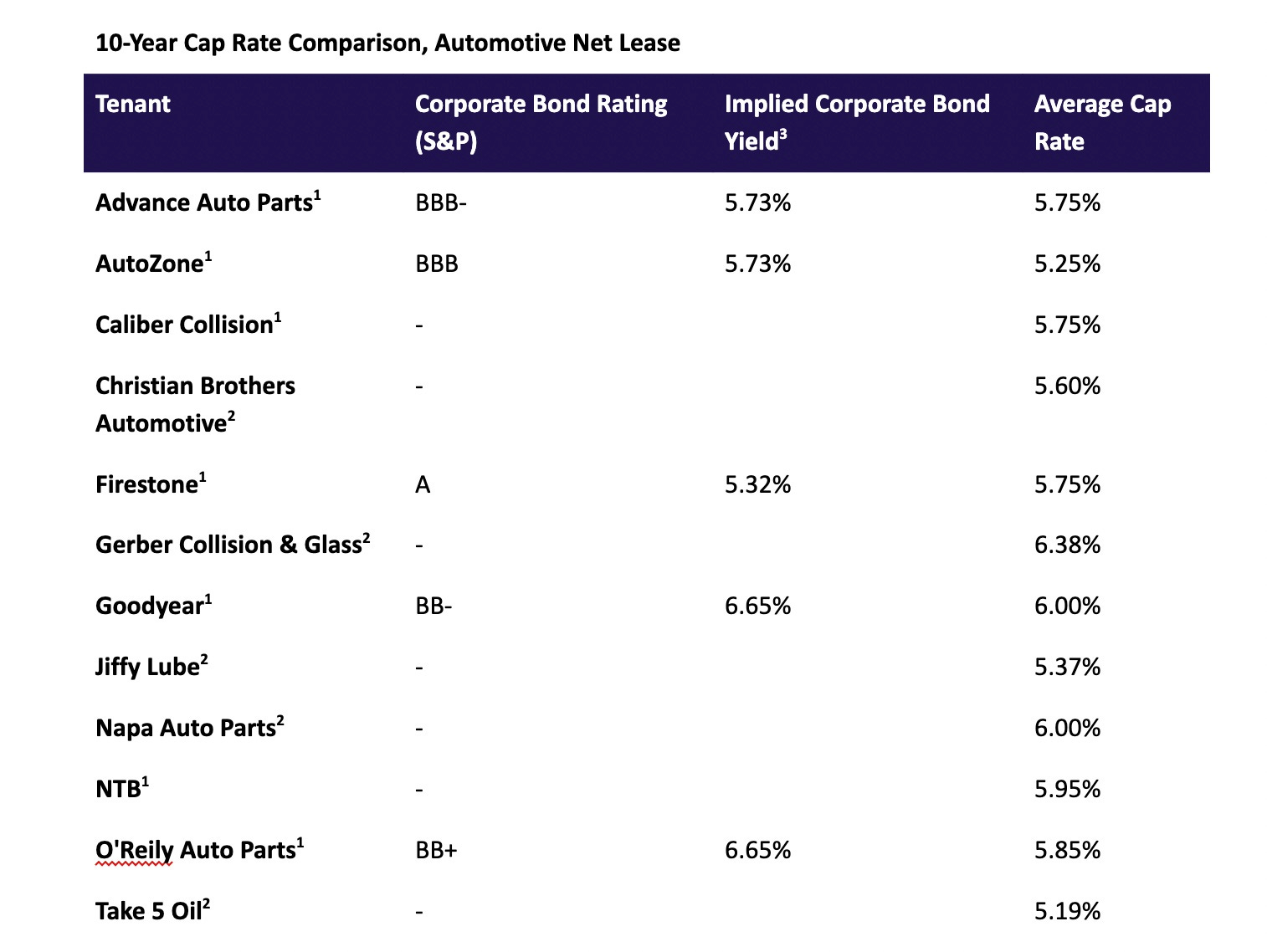

While there are many subsectors within net lease retail to discuss (education, QSR, movie theaters, medical, veterinary clinics, etc.), automotive real estate is a particularly strong opportunity within the net lease sector. While "automotive real estate" covers everything from car washes to dealerships, it is predominantly in auto repair shops where we see such credit tenants as AutoZone, Bridgestone, Jiffy Lube, or Advance Auto Parts. The overall sector represents sizable portions of many portfolios for net lease market leaders, generally in the 5-15% range (i.e. with REITs such as WP Carey, STORE, or NNN).

Credit tenants today are broadly trading in the 5.25%-6.5% range on the open market based on the underlying credit and strength of the operator occupying the space. The below chart articulates both average cap rates, but also articulates the importance of non-core deal origination strategies in today’s market environment (in order to achieve necessary yields above implied corporate bond rates).

The attractiveness of this subsector is largely attributable to four key drivers. First, automotives are an e-commerce resistant sector. As a physical asset that requires ongoing care and maintenance, cars are a part of our everyday lives that need regular attention. Whether in purchasing a vehicle, or keeping it well maintained, human hands must be involved to some degree in that process – or at least the real estate that houses these services.

Second, car ownership rates are on the rise, with Americans owning more vehicles over time.

Our nation is a car-owning culture, a trend supported by high population growth in suburban areas and car-oriented Sunbelt cities relative to dense urban centers in the northeast and California.Third, the length of time Americans keep their old cars continues to grow, averaging at this point around 12 years.

This trend is only encouraged by recent recessionary fears, discouraging people from taking on the rising costs of a new vehicle. This means more repairs, more extra parts, and more need for vendors who can provide these services and materials. While a downside for automotive dealerships, this is simultaneously a boon to auto repair shops which have seen increasing demand.Finally, these three trends culminate in a marked shortage of available labor in the automotive repair space.

Americans are seeing record wait times at auto repair shops as consumers wait for longer and longer periods for their cars to be fixed. While increasing labor costs, this increased demand also translates into higher prices charged to consumers (and likely greater profits for owners of these businesses). Though this might be damaging to customers, it invariably serves as a strong demand driver for automotive repair businesses themselves.Subsector Headwinds and Transformations

While the automotive sector is relatively healthy and resilient, it still does face some potential headwinds. Two primary data points should be considered. First, there is a trend toward electric vehicles and away from traditional combustion engines. Consider President Biden’s target of phasing out the government purchases of combustion vehicles by 2030, and net-zero emissions by 2050.

There are similar bans coming into effect on combustion engine vehicle sales in numerous states including California, Washington, Wyoming, and New York.This presents several issues to the automotive net lease sector, specifically automotive maintenance. First, fewer moving parts in electric vehicles means fewer repairs (i.e. fewer trips to repair shops), and perhaps greater longevity of the vehicles themselves.

Second, the repairs that do need to occur are usually software-based and highly technical in nature, not mechanical. Firms such as Tesla already do remote repair work for their vehicles without customers even needing to take their cars into the shop, resolving up to 80% of reported problems with the vehicles remotely. Finally, EV technology is evolving and gaining adoption at a fast pace, and traditional repair techniques on combustion engines will become increasingly sidelined in an electrified automotive universe.

Yet with the compounding effect of fewer available mechanics and increased car ownership, these headwinds are offset by a bottlenecking of available talent to perform necessary services. Even if electric vehicles ultimately require fewer repairs than their combustion counterparts, with fewer professionals to do the work, and more cars on the road, it potentially nets out to a neutral impact to automotive repair businesses.

What about the risks associated with increasingly complex repairs required for EV vehicles? To the benefit of traditional repair shops, 2021 had seen the passing of "right to repair" legislation at the Federal level in the US. In a move attempting to sidestep the potential for repair monopolies that one sees with firms like Tesla, who try to compel customers to handle all vehicle repairs at the dealership itself, mechanics are learning the newer techniques and technologies to handle late model vehicles.

The second major headwind facing the sector is the impact of autonomous or self-driving vehicles. The potential impact of AVs on American driving culture, land use, and mobility has been discussed extensively. A world of widespread AV adoption– likely to occur by 2050 if not before–will include serious reductions in traffic jams, vehicular accidents, parking, and commute times globally.

It follows that, while cars might still be highly relevant in this AV future, the number of cars required on the road could be reduced as ridesharing provides an increasingly viable alternative for families looking to economize vehicle ownership.However, these trends would require fundamental shifts in consumer behavior to seriously threaten the automotive net lease category. American car culture, increasing car ownership, and movement to more car-centric cities are strong tailwinds. Even if forecasts of an AV future are true, consumer demand and preferences may take decades to catch up. While we can foresee a future where the world needs fewer repairs on fewer vehicles, with today’s trends as they are, it is hard to see a material risk to the automotive industry today.

The Takeaway

Picking a winner is never easy, and many sectors have faced headwinds over the past two years. Yet net lease assets, and the automotive sector overall, provide an interesting opportunity for wealth preservation in a relatively low-risk category. We see increased demand for vehicles and repairs with fewer able-bodied workers to perform them, offsetting the potentially detrimental effects of more EV cars on the road, along with the possible impacts of autonomous vehicles in the coming decades. For those willing to add value in their investment strategies, good deals are still to be found today in the net lease sector; indeed, this might be a once-in-a-cycle purchasing opportunity for those who can brave the current market.

—Jonathan Andrews

NAREIT Investment Performance by Property Sector and Subsector, December 30 2022.

Blue Owl, "2023 Real Estate Outlook," published Q1 2023.

Realty Income Investor Presentation, April 2022: chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://s21.q4cdn.com/421822989/files/doc_financials/2021/q4/Investor-Presentation-April-Update.pdf

https://www.commercialsearch.com/news/2022-net-lease-overall-sales-volume-and-cap-rates/#:~:text=Overall%2C%20the%20net%20lease%20market,points%20to%20continued%20buyer%20demand.

CBRE, "Net Lease Investment Declines Considerably: Q1 2023". May 18, 2023.

NAREIT December 2022

Matthews Real Estate Investment Services, 2023 Net Lease Tenant Report

Matthews Real Estate Investment Services, 2023 Net Lease Tenant Report

Interview with Grant Gaughrin, 7/14/2023

St. Louis FRED, July 19, 2023

WP Carey (6%, 4Q2022 Investor Presentation)

STORE Capital (6%, Form 10Q 9/30/22)

NNN National Retail Properties (17.8%, 4Q2022 Investor Presentation)

https://www.forbes.com/advisor/car-insurance/car-ownership-statistics/#:~:text=National%20Car%20Ownership%20Statistics%20at%20a%20Glance,-A%20total%20of&text=91.7%25%20of%20households%20had%20at,least%20one%20vehicle%20in%202021.

https://www.wealthmanagement.com/net-lease/investment-activity-automotive-net-lease-assets-speeds

https://www.wsj.com/articles/car-repair-shortage-service-e1e06b0f

https://www.reuters.com/world/us/biden-pledges-end-gas-powered-federal-vehicle-purchases-by-2035-2021-12-08/

https://www.utilitydive.com/news/new-york-2035-ban-new-gas-powered-cars-trucks-ICE-vehicles/633041/#:~:text=New%20York%20has%20begun%20the,adopted%20such%20rules%20in%20August.

https://www.nbcnews.com/news/us-news/washington-state-plans-ban-non-electric-vehicles-2030-rcna21683

https://www.usatoday.com/story/money/cars/2023/01/17/wyoming-ban-electric-vehicles-legislation/11067197002/

https://www.acuity.com/the-focus/mechanic/the-future-of-your-auto-repair-shop-with-electric-vehicles

https://www.shop-ware.com/articles/what-will-electric-vehicles-mean-for-auto-repair-shops/

https://www.sfweekly.com/archives/who-ll-fix-your-electric-car/article_e2b8b552-dc4b-520c-a538-911408eb72ad.html

https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/ten-ways-autonomous-driving-could-redefine-the-automotive-world

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them

| A guest post by

|

Start Writing

Start Writing