Loans & co-buying is a classic case of square peg & round hole.

Residential loans are designed for individual (or couple) owners.

Commercial loans are designed for non-resident landlords.

Neither is designed for a group of friends buying property together.

The good news is that you can definitely jam that square peg into the round hole. It just requires a bit of sanding on the edges. We’ll tell you how in this post.

Path #1: Everyone gets on the loan!

Works best when:

There are 4 or fewer borrowers (typical limit for banks)

The ownership group is static over time

Super high trust between the ownership group (each is liable for each other!)

No individual would qualify on their own

How it works

Alice, Bob and Carlton go to a bank. They apply for a loan as a group. They get a loan in all of their names and hold title in their names (can be equal share or unequal share). This is the same as how it would work for a couple, except there are 3 people now.

Be aware #1: Joint and Several Liability

Let us speak of a phrase that lenders and lawyers love. Joint and several Liability!

When you and your 3 friends all get on a loan together, each of you is jointly and severally liable for the entire loan. This means that when Bob flees to Tahiti, Alice and Carlton are fully responsible for his share of the loan payment. The bank doesn’t care that Bob left you high and dry. In fact, the bank can go after Alice and Carlton’s personal assets if Bob doesn’t pay. Everyone, individually, is fully liable for the full loan and the reliability of the others.

Be aware #2: Simple but inflexible

Suppose Bob wants to leave (on good terms) and get replaced by Mary. There is likely no way for Bob to get off the loan. He’s stuck. He can work out a deal with Mary where Mary pays his portion of the loan, but at the end of the day he’s still 100% liable. This structure does not allow for easy changes of ownership.

Path #2: One person gets on the loan

[Note: This could also be a subset of owners, not just one person]

Works best when:

One person/couple has strong financial means and credit

The property produces income (e.g. from rents) to allow that person to make their mortgage payments

How this works:

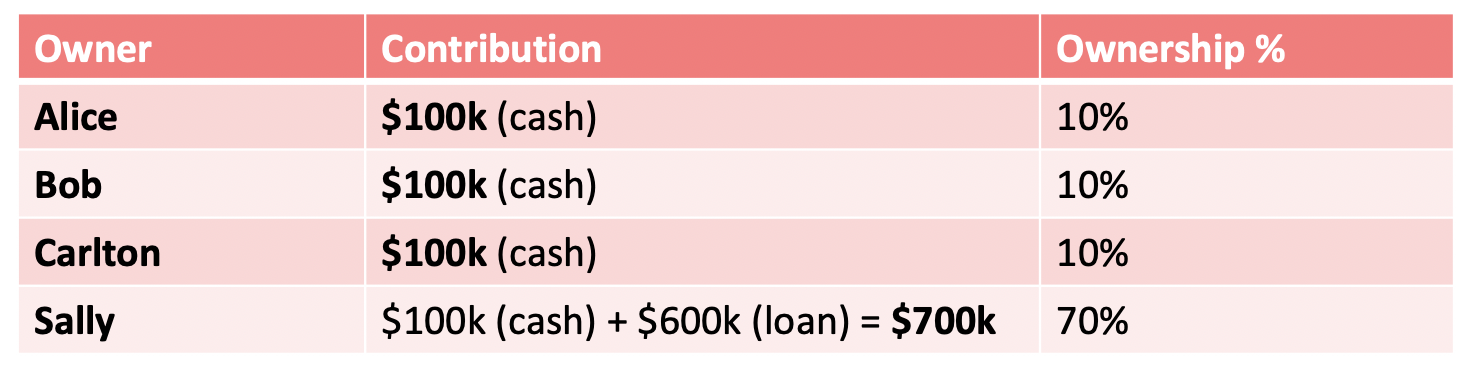

Let’s say there’s a $1m property. You intend to get a $600k loan. There are 4 co-owners, each of whom is going to contribute $100k in equity for the downpayment.

Sally made it rich selling sea shells by the sea shore. She’s going to take on the loan personally. From the perspective of the co-ownership group, the loan is going to be considered her personal cash contribution (the same as if her Uncle loaned her money … the Uncle is just the bank in this case).

Here is how the ownership is then allocated.

Sally owns 70% of the property. Every month Sally will make the entire mortgage payment out of her own pocket.

Usually in this scenario, the property generates some income … most likely from rent. Sally is entitled to 70% of that income. She uses that income to pay off the mortgage. Let’s say the property produces $5k of income each month. Here is how it would get allocated.

Note: Sally is going to make that mortgage payment out of her own pocket. From the bank’s perspective, Sally is the owner of the property and fully responsible for the loan payments. The group needs a side agreement between the individuals that spells out how income from the property is divided.

Path #3: LLC with personal guarantor(s)

Works best when:

You expect ownership to change over time. People will buy in and sell out.

There is a personal guarantor(s) with strong financial means

Your lender is willing to have you take ownership in an LLC (some do, but not all)

The property produces income (e.g. from rents) to allow the LLC to make its mortgage payments

Banks don’t lend to naked LLCs without track records. Imagine you are a bank. Someone created an LLC yesterday. Would you lend money to this fictitious entity they just created? Of course not. The LLC could just walk away with no consequences whenever.

Banks want someone with real assets they can go after. Banks will lend to an LLC (not all banks, but some) IF there is a personal guarantee from an individual. This means if the LLC defaults, the individual is responsible for the loan payments.

You might ask… what’s the point of the LLC if there is a personal guarantee behind it? Well, the LLC structure allows you to flexibly have people buy in and sell out without changes to the title.

The title (something kept by the city or county) will just say "Your LLC."

Meanwhile, you will be keeping side records of who owns the LLC, and this can change over time without the city/county getting involved.

This also allows the LLC to build credit, which comes in play for Path #$ 4.

Compensation for the guarantee?

The personal guarantors might do it to "make the project happen" and not need any compensation. We commend this, but realize it might not always be possible.

The guarantors also might ask for some compensation for the risk they are assuming. How much compensation is appropriate? One article suggests 1-10% of the value of the loan, but this decision is likely to be deeply personal and context-specific. Compensation could also take the form of reduced rent, extra decision-making rights, extra equity along the lines of Path #2 above, etc.

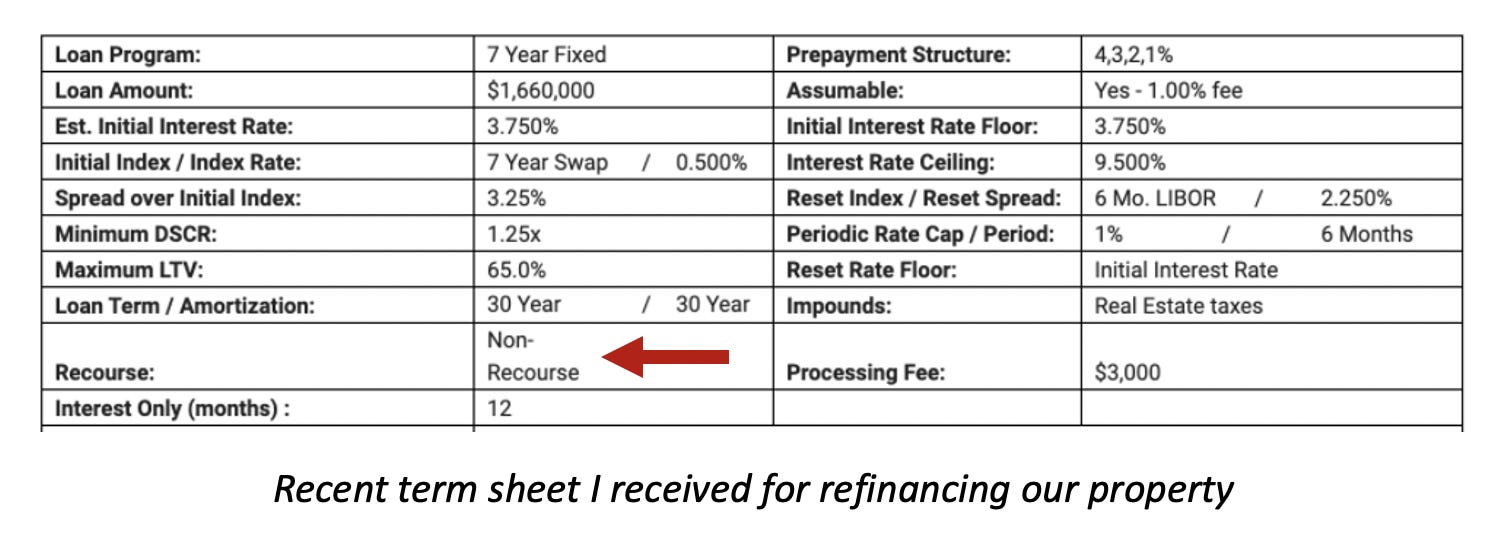

Path #4: Refinance later into a "non-recourse" loan

Works best when:

The property generates solid and stable income (e.g. from rents)

Interest rates are stable or decreasing since purchase

The property is originally held as an LLC

This one, mechanically, is a bit trickier but I actually like it quite a bit.

Essentially you are going to start with path #3, but swap out of it later.

Above we said that banks don’t lend to a naked LLC without a track record. Well, suppose everything goes well. It’s 2 years later, your community is stable, rents are coming in. Ladies and gents, that’s what we call a track record!

With a stable 2-year history, a bank now may be willing to lend directly to your LLC with no personal guarantees (called a "non-recourse" loan). You can refinance your original loan with this new loan. And now, no single individual is on the hook for the loan.

The bank will want to see a stable operating history. The key metric they will look at is "Debt Coverage Service Ratio" or DSCR. Banks I’ve spoken to recently have been asking for a ~1.25x DSCR. That means if the loan payment is $100k per year, they want to see a net income (revenue minus expenses) of $125k.

Doing one thing to get the project off the ground with plans to swap it out for something more stable (and less personally liable) can be a good plan for co-buying property. Real estate developers do this frequently with short-term "hard money loans" that have high interest rates, but looser requirements. They pay a high rate for 1-3 years during a risky part of the project and then refinance the loan into a more stable permanent loan once things are stabilized. I’m not recommending hard money loans for folks co-buying property (they are very risky) but this two-step process is fairly common.

Path #5: Each person finances a portion of the property (e.g. condo)

Works best when:

Purchasing a subdivided property (e.g. condo, TIC)

People own the space they live in on the property

The above 4 paths assume there is a single "parcel" that people own together. There are some types of properties where people can own a piece of the property individually. The most common property type here is a condo. Each individual could own a unit in the condo building and get a loan for their unit individually. Easy peasy.

The same is true if you are buying 2 houses next to each other. Each person can own a house, finance it individually, and then have a HOA agreement that specifies how the space is shared between people.

This is a great option under very specific circumstances, but will not work for most properties or ownership arrangements.

Your experience?

We’d love to hear about your experience talking to lenders. What’s worked? What hasn’t? Are there any paths we are missing?

Leave a comment or email us at [email protected]

Subscribe to Supernuclear

Launched 2 years ago

A guide to coliving

Publish on Substack

Publish on Substack