Five Ways New Real Estate Concepts Are Getting Funded Today

With fewer venture capital deals getting done, entrepreneurs innovating in the built environment are finding capital in new places.

Thesis Driven dives deep into emerging themes and real estate operating models by featuring a handful of operators executing on each theme. This week’s letter the first of a two-part series digging into the future of financing models for new real estate companies.

The past ten years saw many new real estate concepts come to market, from managed office to short-term rentals to new ways of buying and managing single-family homes. Many of those companies were backed by traditional venture investors, and a few of them even went public with technology-like stories and valuations.

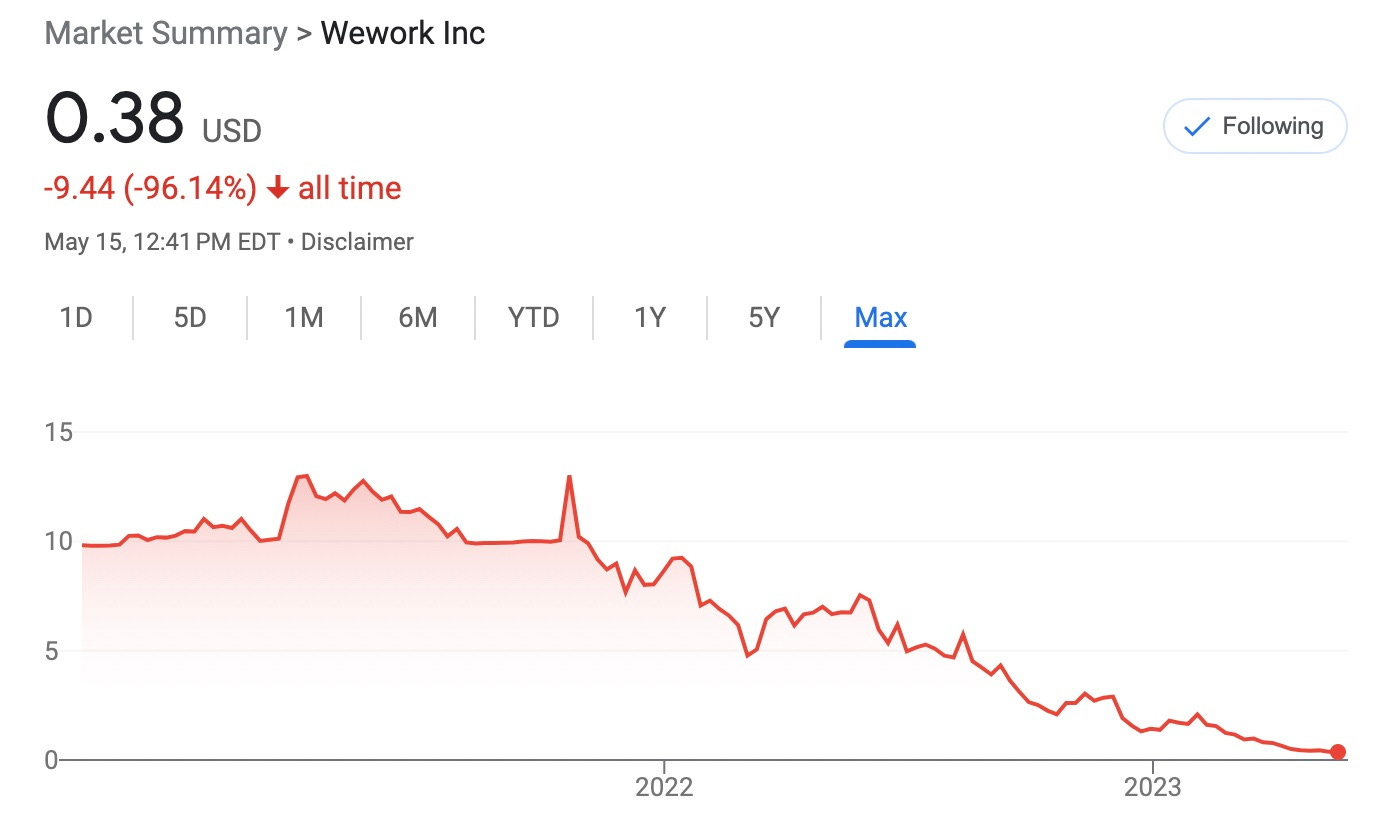

But over the past 12 months, the picture has gotten ugly. WeWork and OpenDoor, perhaps the two best examples of venture-backed real estate-related companies with financial or operating (rather than technological) innovations, are currently trading for a combined market capitalization of approximately $1.5 billion, more than an order of magnitude below their total funding raised. Companies like Sonder are fairing even worse; their current market cap is a mere $90 million.

I don’t believe these are bad concepts or even bad companies. The physical world is in need of creativity and innovation, and immense wealth can be built through real estate. But novel real estate business models are rarely technology companies, and venture capital is often the wrong vehicle to finance this kind of enterprise. Unfortunately, there aren’t many obvious financing alternatives for real estate entrepreneurs—but that’s beginning to change.

Today’s letter will dig into five ways that these concepts are going to get funded in the future across various stages of development from idea to scale. For each, we’ll dig into the typical structure, when and where it might be appropriate, and identify some examples of investors doing deals today.

OpCo-PropCo Structures

Co-GP Investments

Real Estate GP Incubators

Strategic Partnerships

Private Equity and Alternatives

1. OpCo-PropCo Structures

As regular Thesis Driven readers know, we’ve written about OpCo-PropCo structures extensively in the past. We’ve covered various OpCo-PropCo models and future directions for the category, and we also maintain a list of investors who do OpCo-PropCo deals.

In an OpCo-PropCo structure, an investor backs an operating company (OpCo) in addition to making an investment in the assets managed by that company (PropCo). Done right, the structure can be a win-win: the investor can participate in financial upside on both sides of the transaction while the operating company gets an accelerant beyond a typical venture investment.

For many reasons, an OpCo-PropCo structure can be a better fit than venture for a brick-and-mortar business. With a dedicated pool of "PropCo" capital, the operating company can avoid sinking expensive venture dollars on real estate expenses. The structure also aligns interests between the operator and investor; an investor with a meaningful stake in the real estate is unlikely to push an operator to grow so quickly that operational quality suffers.

Distinguishing the OpCo and PropCo can also help entrepreneurs bridge the gap between typical venture terms and real estate financing terms, as the latter can be far less entrepreneur-friendly. With a dual structure, real estate investors can have the protections, upside, and rights they need in the real estate venture while the entrepreneur (GP) retains control of the operating business.

Of course, OpCo-PropCo arrangements can run into hairy structuring challenges, and potential conflicts of interest must be addressed. Last year Kunal Lunawat at Agya wrote an excellent overview of the structure and some of its challenges here, including common questions regarding OpCo-PropCo economics and governance.

Despite these challenges, more investment firms are bringing OpCo-PropCo financing vehicles to market. Several investors—including 1Sharpe and Alpaca—explicitly pitch their ability to invest in operating companies as well as those companies’ underlying real estate assets. And many more investors, especially those with hospitality experience, have the ability and willingness to do OpCo-PropCo deals when it makes sense, especially once a real estate concept moves beyond proof-of-concept.

2. Co-GP Investments

Innovative real estate companies often require significant capital before they are ready to seriously approach real estate LP investors. Real estate LPs usually expect a GPs to approach them with a development-ready site pre-vetted, under control, and (in many cases) entitled. And once an LP decides to invest, he or she expects the GP to put up even more capital—usually 10% of the total project cost.

As many entrepreneurs have discovered, these GP investments are not a great use of venture capital dollars. Fortunately, there’s an existing structure that real estate GPs have employed for decades: co-GP investments. In these investments, a real estate entrepreneur brings on a GP partner, giving them a share of the upside (promote) in exchange for capital and—perhaps—connections to LPs. Jonathan Livi provides a great overview of the different type of real estate co-GP investors over at Lev.

Of course, co-GP capital isn’t cheap; in many cases it’s more akin to bringing on a co-founder than taking a round of seed capital. After all, many co-GP investors don’t just bring money but expertise, experience, and a track record. For entrepreneurs without development experience looking to innovate in the built world, bringing in a co-GP partner can be a powerful accelerant and significantly de-risk a venture. If one wouldn’t blink at bringing in a software engineer as a co-founder for a software company, why scoff at bringing on a veteran developer to a real estate company?

The past decade has also seen the rise of co-GP funds such as Milestone Partners and Security Properties as well as other vehicles to help entrepreneurs finance their GP investments, particularly if they don’t want to have a venture-backed OpCo. However, it is important to note that many LPs view a GP’s over-reliance on third-party GP capital a negative signal, as they see the GP’s 10% investment as "skin in the game" irrespective of the GP’s ability to put up that capital.

So while third-party co-GP funds are a viable option for real estate entrepreneurs looking to fund their GP commitment or lock up sites, many founders would be better served by bringing on a co-founder with some capital and experience willing to serve in a co-GP capacity—and ideally, co-sign construction loan guarantees. This would be the "true partner" co-GP highlighted in Livi’s article; this kind of co-GP is almost always an individual, not a firm.

3. Real Estate GP Incubators

Last month, Adaptive RE founder and Twitter personality Moses Kagan announced the creation of a new kind of incubator: ReSeed Partners. Together with his co-founders Rhett Bennett and David Bergeron, Kagan is piloting an incubation model that combines mentorship and shared services with co-GP and LP seed capital to help aspiring real estate entrepreneurs get their businesses off the ground.

ReSeed is notable in that it is looking to incubate new real estate development firms, not venture-scale startups. Rather than investing in operating companies, they’re making co-GP investments into firms while bringing LP investors into individual deals. Specifically, they’re looking to find aspiring real estate entrepreneurs with deep local knowledge in a specific market—think analysts or associates at real estate private equity firms, brokers, architects, and contractors—and pair them with mentorship, services, and capital.

While ReSeed is fairly unique today, it is unlikely to stay that way for long; incubators and accelerators for startups proliferated after the early success of YCombinator over fifteen years ago. And I wouldn’t be surprised if some new incubation models sought to combine the best of ReSeed with venture accelerators, appealing to real estate entrepreneurs with ideas too wacky for ReSeed but too grounded in sticks-and-bricks for TechStars.

Aspiring real estate entrepreneurs would be wise to look to these incubators as a way to get a running start as well as valuable real estate experience and guidance. ReSeed’s investment model—providing co-GP capital rather than a venture seed check—is also likely a better fit for most new real estate concepts, as it doesn’t force companies onto a "venture track" with the expectation they’ll raise a Series A at a high valuation in twelve to eighteen months.

4. Strategic Partnerships

Finding an aligned strategic partner or customer willing to bankroll your company’s development is one of the most tried-and-true ways to bootstrap a startup. And with the venture market cooling, I expect more entrepreneurs to look to strategic partnerships to get their real estate concepts off the ground.

While this path can take many forms, it usually entails an early-stage company finding a customer or partner with a need that is "close enough" to what they would like to build. The company then works closely with the client to build and polish the product, whether it’s a piece of software or a real estate concept. The partner then becomes Customer #1 for the entrepreneur’s company, likely with special attention and support in exchange for agreeing to act as a reference for future clients.

For example, I’m close with one real estate technology company scaling successfully through a partnership with a (non-real estate) Fortune 500 customer. While specific customizations and product work were needed for that client, the entrepreneur is free to sell the broader platform to other customers as long as they are not competitive.

But this path can come with significant downsides. As an entrepreneur, you’re wholly reliant on your client or partner, and shifting political winds within their organization can doom your company. The partner may also expect certain exclusive rights to the product and its derivatives; entrepreneurs would be wise to negotiate this up-front to avoid a nasty surprise down the road. And while this path is seen as "non-dilutive," many entrepreneurs choose to give some equity—or investment rights—to their first client or partner to align interests.

This kind of structure also has a fuzzy overlap with OpCo-PropCo structures. An exclusive PropCo partner that also makes a significant investment in the operating company—think Iconiq’s deal with Sentral+—can look a lot like a strategic partner or even acquirer.

5. Private Equity and Alternatives Investors

Alternatives investors and hedge funds have historically had interest in innovative real estate concepts and companies but haven’t been investors of choice for entrepreneurs given those firms’ tendency to be price-sensitive and founder-unfriendly. But with venture investors less eager to fund sticks-and-bricks concepts, alternatives investors may deserve a second look.

Of course, these firms haven’t been totally locked out of the proptech investment market. For example, Rialto Capital was a main backer of Hello Alfred’s purchase of RKW while Davidson Kempner backed PlaceMakr, neither of which were structured like traditional venture investments. Real estate-friendly alternatives investors like Fortress and TPG have also both been involved in new built-world ventures, and TPG just raised another $7 billion in opportunistic real estate capital.

Unlike seed-stage VCs or co-GP investors, these firms are unlikely to invest at the earliest stages of a new venture. Instead, they’ll typically want to see a few examples of the concept at work before jumping in. But unlike many early-round investors, they can bring larger checks to the table without the laborious process and extended diligence that an institutional investor would bring, and many can invest across both OpCo and PropCo structures.

It is important to remember that these firms worked hard to earn their reputations of being expensive, unfriendly capital. Traditional private equity firms and hedge funds love to add structure to deals, and they’re not afraid to put very investor-friendly terms on the table. In addition, they often view tough times or challenges as an opportunity to squeeze better economics out of a deal—to the detriment of management and early investors—rather than offer support. But that approach to business is far more pervasive in real estate than in venture, which may come as an unwelcome surprise to many proptech entrepreneurs.

Coming to Terms with Real Estate Terms

Founders familiar with venture rounds—particularly the kinds of deals getting done over the past five years—will likely be disappointed by the relatively investor-friendly norms of the real estate world. In comparison to venture investors, real estate LPs tend to command more control and capture far more of the upside in a particular deal than even the most predatory VC. This isn’t simply a matter of differing norms driven by sharp-elbowed real estate types; real estate investors generally have less upside than startup investors while also having a hard asset they need to protect.

For example, a typical real estate deal might see an LP investor earn an 8%-per-year preferred return along with 80% of the upside beyond that 8%. In venture terms, this would be akin to a seed investor asking for 80% of the company on a participating preferred equity investment with an 8% coupon, a structure unheard-of in polite tech circles since at least 2009. Of course, a real estate LP will also ask for control rights over major decisions much more extensive than would be seen in a typical venture deal.

Of course, we’re describing two different deals with different investors needs and risk/return profiles. But we’re comparing grapefruit and oranges, not apples and oranges, especially since many entrepreneurs with real estate-style deals who have been happily taking venture money for the past decade are now looking to the real estate capital markets for funding. Expectations should be set appropriately.

These categories of investment aren’t mutually exclusive, and they often overlap. An entrepreneur may also choose to capitalize their business with one structure at the early stage and move to a different capitalization structure later on, just as startups evolve from taking friends-and-family money to venture capital to tapping the public markets. For example, it’s reasonable for a real estate venture that starts out with a co-GP partnership to cash out that co-GP later on with capital from a strategic investor or alternatives group.

Of course, the five categories I covered here aren’t the only paths for an entrepreneur looking beyond venture capital. Public sources of financing get less attention than they should, and occasional Thesis Driven contributor Fed Novikov is actually working on a company trying to change that. Family offices can also be an answer for entrepreneurs with an concept off the beaten track, although given their diverse interests and investment profiles family offices and high net worth individuals are difficult to paint with a broad brush; you just have to meet the right one at the right time.

Too often, entrepreneurs and investors alike get tripped up by terminology. "Proptech" as a concept is broken; it lumps Sonder with VTS and WeWork with Placer, businesses that share little in common beyond being grouped into the "real estate technology" sector. Part 2 of this series will dig more into the challenges of "proptech" and a path forward for entrepreneurs looking to bring new concepts to the built world.

—Brad Hargreaves

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them

Start Writing

Start Writing