The Future of the Property Management System

Platforms like Yardi, Entrata, and AppFolio are at the center of real estate tech. But key questions around AI, platform openness, and upstarts loom on the horizon.

No piece of technology is more essential to the real estate industry than the property management system.

While many proptech tools innovate on the margins, the bulk of software dollars in real estate end up in the pockets of the companies running property management systems such as Yardi, AppFolio, Entrata, RealPage, and MRI. These companies have proven highly resistant to disruption over the years; MRI was founded in 1971, Yardi in 1984, and RealPage in 1998. AppFolio, the baby of the bunch, was launched in 2006—the same year Facebook expanded beyond higher education and Apple sold the first MacBook.

But there is reason to believe that change may be coming. Recent years have seen several new entrants raise significant capital to take on the incumbents. Customer expectations are also changing, with large real estate owners less tolerant of walled gardens in which "good enough" is sufficient.

Today’s letter will explore the future of the Property Management System, including:

The current PMS landscape and existing operators, including interviews with executives at AppFolio and Entrata;

Industry dynamics and moats;

Challengers and new entrants, including interviews with several venture-backed founders taking on the space;

A long (10+ year) view of the evolution of the PMS landscape in the context of other industries’ trajectories.

What is a Property Management System, Anyway?

At its core, the property management system is an ERP: an Enterprise Resource Planning tool. This is a broad and wonky category of business management software; outside of real estate, major ERPs include Oracle’s NetSuite, Microsoft Dynamics 365, and SAP ERP. While ERPs can manage a wide range of business processes, they are most commonly responsible for finance and accounting, inventory management, business planning, procurement, and supply chain management.

ERPs serve as a "single source of truth" for large organizations, holding any and all information around financial performance, inventory, orders, supply chain, and more. Many organizations also use their ERP to manage HR matters, payroll, work orders, and even customer relationships and marketing.

For those peripheral categories, organizations often must make a choice between ease of integration and functionality. Salesforce is very likely a better CRM than Microsoft Dynamics 365’s built-in CRM, but a Finance team might argue that Dynamics’ CRM is Good Enough and the data integration is far easier. For example, if the company uses Dynamics for both accounting and CRM, then associating purchase orders and payments with specific customers is much simpler. Sales, of course, is likely to object, arguing that Dynamics is an inferior CRM and they all used Salesforce at their last jobs.

I go into this detail not because I’ve experienced this exact conversation—although I have—but because it becomes really important later on when we discuss the dynamics of the PMS market and analyze the threats facing incumbents.

Property Management Systems have a set of modules analogous to mainstream ERPs but adapted to real estate. For example, PMS platforms have their own accounting software, CRMs, inventory management tools, and much more. And like mainstream ERPs, many of those PMS modules were acquired through M&A rather than built in-house. For example, RealPage’s acquisition of revenue management tool LRO in 2017 for $300 million was one of the largest proptech acquisitions to date.

Compared with the rest of proptech, the biggest PMS companies are tremendously large and profitable. While the largest PMS companies are private—and therefore do not publicize their revenue—Yardi, the largest management system, is estimated to generate well over a billion dollars of high-margin revenue per year. Even a smaller platform like Entrata was able to command a $507 million round of financing in 2021 while boasting a revenue run rate in excess of $200 million.

PMS companies’ size, profitability, and hunger for new modules and products to sell to their existing customer base has made them some of the most acquisitive players in all of real estate technology. RealPage and Yardi each usually make one to three acquisitions per year, and they’ve bought some notable proptech names in recent years including KnockCRM (RealPage, 2022), Planimetron (Yardi, 2022), Buildium (RealPage, 2019), Dynasty (Appfolio, 2019), and Rentlytics (RealPage, 2018).

But despite all the acquisitions, the PMS landscape remains frustratingly static for many users.

The Incumbents

Before we dive into the dynamics of the PMS sector—and the reasons why change has been slow to come—it’s worth spending a bit of time on the major PMS players across a few broad categories:

Yardi

With over 13 million units on its platform, Yardi is by far the largest property management system and deserves a category unto itself. Yardi was started by one man, Anant Yardi, a programmer and first-generation immigrant. As far as I am aware, Yardi has taken no outside capital and is still entirely owned by Mr. Yardi.

On the spectrum of property management systems, Yardi skews institutional with a majority market share among large owners and investors. Yardi is generally seen as the most advanced property management system on matters of accounting and reporting, and—in comparison to its peers—has built many of its modules in-house rather than adding them through acquisitions. That said, Yardi’s consumer-facing products, such as its marketing tool and resident app, RentCafe, generally receive poor reviews and are the frequent target of proptech point solutions.

Yardi is also known for being litigious and has sued its PMS competitors for various reasons at various times, including RealPage, Entrata, and RealPage (again).

Other Established PMS Systems: MRI, RealPage, RentManager

As mentioned earlier, Yardi isn’t the only property management system that has been around for a very long time; it’s just the most successful. RealPage, MRI, and RentManager—along with a few even smaller players—are all at least 25 years old. While smaller than AppFolio, these players—especially RealPage and MRI—have substantial adoption among institutional owners and cannot be ignored as major players in the PMS landscape.

RealPage in particular is very acquisitive, with many of its modules—including its very successful revenue management applications—having come through acquisitions. Many owners, for example, use RealPage’s revenue management tools on top of Yardi’s property management system; RealPage even puts out press releases touting their integration with Yardi, their largest competitor.

"Emerging Incumbents": AppFolio and Entrata

At risk of coining an oxymoron, I can’t find a better way to describe AppFolio and Entrata than Emerging Incumbents. These are not new players—Entrata is 20 years old and AppFolio is 17—but they are relatively young on the spectrum of PMS players and are bringing more startup-like approaches to the sector.

I spoke with Stephanie Fuhrman, SVP of Corporate Development at Entrata, for this letter. Fuhrman has a rich background in real estate technology; she was formerly the Managing Director of Global Innovation at Greystar, the largest property management firm in the United States. "Since Silver Lake invested, joining Entrata felt like going to a startup again with a fresh perspective," said Fuhrman.

Like Yardi, Entrata’s customer base trends toward larger owners. "Our existing customer base is [owners of] 1,000 units up to the largest owners / managers in the industry," noted Fuhrman. By tackling the institutional segment of the market, Entrata is taking on Yardi and the PMS incumbents directly.

AppFolio, on the other hand, has found success by targeting smaller owners. "We originated in the SMB sector and thrived there," notes Matt Baird, SVP Engineering at AppFolio. The strategy has been a success, with AppFolio growing into the second-largest PMS platform with approximately 7.8 million units. "But lately, our success has significantly expanded into managing large multifamily portfolios," he adds, speaking to their expanded focus.

On the spectrum of PMS companies, AppFolio has also been relatively tech-forward, particularly in its use of AI to automate workflows. In October of this year, the company announced RealmX, a product that allows property managers to communicate with AppFolio via plain English commands rather than series of specific workflows and commands—long a driver of PMS systems’ steep learning curves. "Shavings make a pile," said Baird. "Many small innovations lead to big improvements, empowering our customers to operate more efficiently."

The PMS Doldrums

A number of years ago, I attended a conference organized by a large institutional owner for their third-party managers. The stated goals of the summit were (a) for property managers to share best practices and learnings with each other and (b) for the owner to better understand how they could help their property managers succeed.

They did not need an in-person gathering to achieve the latter. Overwhelmingly and repeatedly, managers expressed years of pent-up frustration at Yardi, the owner’s chosen property management system. Universally, the management companies had one suggestion to make their lives easier and their properties better: fix or replace Yardi.

I don’t believe much has improved since. To the best of my knowledge, the owner has not replaced Yardi. And when I chat with other owners and managers, they still regularly complain about their property management systems—they’re confusing, slow, cumbersome, and don’t work well with separate parts of their own platforms, let alone third-party tools. This problem isn’t unique to Yardi; other major legacy systems get similar heat.

And integrations with third-party tools is the point where most real estate property management systems begin to diverge from their ERP cousins. While ERP companies like Oracle and Microsoft have embraced their roles as a hubs in a network of third-party applications, major PMS platforms have a complicated relationship with third-party software.

The expectation that most customers from outside real estate would have from a "source of truth" platform—that there are straightforward, automated ways to get data in and out—is not met by most major property management systems. This adds another layer of frustration to clients as well as a serious barrier to new proptech point solutions. We’ll dig into this in more detail later in the letter.

But given the high level of interest and investment in proptech over the past decade, why hasn’t something better emerged?

Moats, Moats, Moats

Property management systems benefit from tremendous lock-in. Once a real estate owner has decided to embrace a PMS platform, it is incredibly difficult to leave.

It would be incorrect to attribute this to real estate owners’ unwillingness to embrace new solutions. For example, even the most forward-looking, tech-savvy owners operate on Yardi. For example, consider this job description for a Yardi administrator from Flow, Adam Neumann’s Andreessen-backed apartment brand. If any apartment operator should be embracing an up-and-coming, open, tech-forward PMS, it should be Flow—but they’re not.

And many new, innovative real estate management concepts start out on a smaller PMS (or their own homegrown PMS) only to end up on Yardi or RealPage as they grow. My own Common, for example, spent its first five years on a homegrown PMS. But as we grew and took on larger property management clients, we faced more unique situations that called for PMS functionality that didn’t feel core to our business. Maintaining compliance for different types of rent-controlled units and serving bespoke owner financial reporting requirements, for example, would require heavy engineering lifts on our own team but would come out of the box with any major PMS system. So after an extensive research process, we threw in the towel on our own system and moved onto Entrata.

The mechanics of real estate capital stacks are a major part of incumbent PMS moats. For example, many institutional allocators will use a specific property management system’s asset management tool to oversee their entire portfolio. That tool will produce reports in a certain format that become familiar to asset managers, executives, the firm’s investors, and lenders alike.

The allocator’s chosen PMS tool will also be able to produce roll-up reports that aggregate and compare data across different properties. While it is technically possible to funnel property data from one PMS into another—say, from MRI into Yardi, or vice versa—it’s not easy, very susceptible to errors, and requires constant maintenance. Therefore, there’s a strong pressure from large investors to keep all their properties on one PMS, making experimentation difficult. Large owners can’t do a single-asset "pilot" of a new PMS.

So even though Common was now on a "mainstream" PMS—Entrata—our challenges were not over. Many of our large clients expected property-level reporting in their Yardi system, so we had to build and maintain special integrations to get data from our Entrata into their Yardi. And even smaller owners without a centralized asset management platform—but other properties on Yardi—expected to see property-level reports in the standard Yardi format. None of this is impossible, but it all requires engineering work and is exceptionally prone to breaking.

And the moats aren’t just top-down; there’s on-the-ground resistance to PMS migration as well. "You have this massive population of accountants who just know how to do stuff in Yardi," notes Dom Beveridge, multifamily industry expert and the author of 20for20, an annual multifamily industry report. "Any deviation from Yardi is going to risk adding complexity, disrupting accounting processes and, ultimately, roles." Beveridge shared an anecdote of one multifamily operator who ran a bake off between Yardi—the incumbent—and AppFolio. While the business was compelled by AppFolio's vision, the incumbent won the bid after facing an internal revolt from its accounting department.

This resistance has shaped how newer, more user-friendly products like Entrata get used. For example, some large owners—such as AMLI, for example—have found success with an "Entrata in the front, Yardi in the back" model: Entrata is used for all tenant-facing property management tasks while Yardi remains the source of truth for property finances, accounting, and reporting. "[Property managers] often prefer the Entrata UX over systems like Yardi or RealPage," said Beveridge. "But that typically entails a trade-off in areas like data analytics, as the bigger platforms have more sophisticated reporting and analytical capabilities at this point."

While this kind of split arrangement is viable, keeping the integrations working and data flowing can be a challenge. For example, both systems need to know about unit vacancy, pricing, discounts, and tenant applications. If the pricing of a unit is changed in the tenant-facing marketing system, this must be communicated to the accounting system for accurate reporting. While this may not seem like a tremendous technical challenge, PMS APIs are notoriously finicky, and Entrata and Yardi are direct competitors with a history of litigation between them. Mashing them together takes work and is inherently fragile; the fact that savvy institutional owners do it speaks to Yardi’s extraordinary lock-in as an accounting platform.

The Ecosystem Question

Over the past fifteen years, it has become increasingly common for popular B2B software products to re-envision themselves as platforms. While a software product is simply bought and used by its customer, a software platform can connect products built by other, third-party companies. Take Salesforce, for example: rather than simply being a CRM that a customer can purchase and use, Salesforce hosts a marketplace with over 4,500 third-party apps. Each of these apps integrate with Salesforce and can help Salesforce’s customers do things they wouldn’t be able to do with Salesforce alone—run custom email campaigns to their Salesforce contacts, integrate Salesforce with their reporting system, or visualize Salesforce data using BI tools, for example.

While some AppExchange apps are free, most are either paid or lead back to paid or freemium products. And AppExchange is wildly popular, with over 90% of Salesforce customers using at least one AppExchange app. Salesforce takes its cut, of course, charging developers 15% to 25% of the revenue they generate on AppExchange.

But while AppExchange generates meaningful revenue, the direct financial benefit is only one reason why software companies love building platforms. Controlling a platform entrenches a company as the clear winner in a market. Potential competitors don’t just have to surpass the incumbent’s functionality, they have to surpass the entire ecosystem’s functionality. A startup looking to challenge Salesforce doesn’t just have to build a better CRM—that’s the easy part—they have to replicate an ecosystem of thousands of third-party apps and integrations.

As an entrepreneur, I’m not going to pick Salesforce because it’s the best CRM. I’m going to pick Salesforce because it integrates with everything. My ERP, my marketing platform, my data warehouse, my BI tool, my analytics platform, some AI tool my CMO found, and pretty much any other long-tail B2B app I want to try out. That is a tremendous moat.

Salesforce isn’t the only company that has won a market by building a robust platform for third-party apps. Marketing software company HubSpot is another example, with a $25 billion market cap driven by a platform with over 1,000 third-party integrations. Remen Okoruwa, Founder & CEO of Propexo (formerly Propify), was a Senior PM at HubSpot before leaving to bring a platform orientation to the property management software world.

"In other industries, most people don’t stress out about 3rd party integrations," said Okoruwa. "Software incumbents are API-first. They have robust APIs that work really well with teams supporting those API programs."

In comparison to industry standard software platforms—a Salesforce, Hubspot, or Twilio, for example—PMS platforms tend to differ in a few major ways:

API technology. While modern technology platforms use REST or GraphQL APIs, most PMS systems use SOAP, an API protocol developed in the 1990s. SOAP is far more rigid than REST, and many software engineers are unfamiliar with SOAP.

Up-front fees. While it’s not uncommon for platforms to charge developers a fee—usually a percentage of revenue or usage-based—many PMS companies have implemented steep up-front charges ($10,000 or more) to any developers looking to integrate.

Paywalled documentation. While many software platforms put their API documentation on the web for all to access, property management systems generally only allow developers to access documentation once they’ve paid an entry fee (see above) and been approved. "You don’t know what you’re getting into until you’ve already paid," notes Okoruwa.

Furthermore, PMS APIs have the reputation of being fragile, buggy, poorly documented, and prone to breaking when seemingly-innocuous software updates are rolled out. An integration with Salesforce can be built by a junior software engineer over a weekend; an integration with Yardi can take a talented and experienced team months.

While successful software platforms in other industries have embraced their roles as hubs serving a broader ecosystem of apps and tools, incumbent property management software platforms have done so only begrudgingly. And there is a fundamental conflict inherent to the "platform" role: in order to cultivate an ecosystem of third-party apps, a platform must cede some degree of both control and revenue. By choosing to allow third-party developers to build apps on top of a platform, the platform is granting those developers the ability to exert their own creative control over a product that touches the platform’s users—as well as monetize those users. Different tech platforms have varying constraints on third-party developers; for example, Apple famously forces third-party developers to work within tighter bounds than Android.

Furthermore, a platform must have a sense of what is "core"—that is, the functionality controlled and monetized by the platform—and what is up for grabs to third-party developers. PMS platforms have struggled with this distinction. Historically, PMS platforms been full-service, offering every module a real estate owner would possibly need in-house. Therefore, many third-party apps didn’t explicitly add functionality, but rather did things the PMS platforms already did, but better. This meant that third-party apps were seen less as complements and more as competitors.

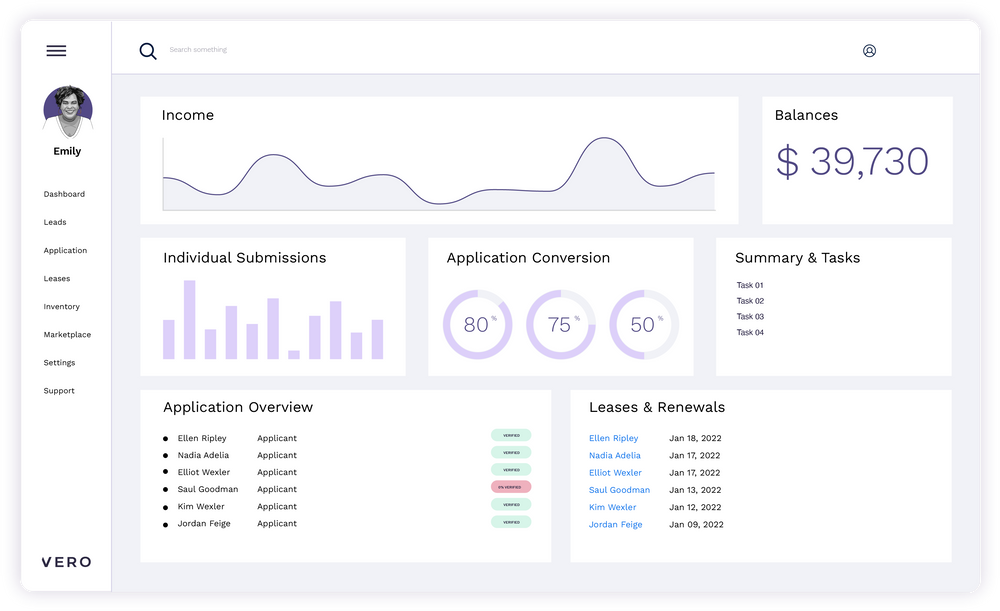

Vero, a tenant screening tool, is a great example of a product with a complicated relationship with its PMS partners. Lou Baugier, the founder & CEO of Vero, explained the nuances to me. "We compete against the PMS platforms every day of the week. We are direct competitors, but we don’t exist without their partnership. It’s a competitive relationship that’s mutually respectful."

By providing operator-customizable tenant assessments, Vero has been able to win impressive clients including Gables, Camden Property Trust, LeFrak, and TF Cornerstone. In theory, PMS platforms provide (and charge per-use for) this same tenant screening functionality. But just as Microsoft Dynamics’ CRM isn’t as good as Salesforce, the out-of-the-box PMS modules are often inferior to purpose-built point solutions like Vero. For a critical function like tenant screening, owners will often choose to go with the better, standalone solution, taking away fees that would have otherwise gone to the PMS.

But for a standalone solution, integrating with property management systems is critical. Without the ability to automatically view new tenant applications—and post their screening reports back to their clients’ PMS—Vero would be far less useful. "There are so many different teams dependent on what Vero does. Accounting, marketing, leasing, asset management, and even the executive team," said Baugier. "Your capability or capacity to integrate well with PMS is difference between winning a major operator and losing. We pay a lot of money to integrate with them."

Today, Vero integrates with all major property management systems, a major accomplishment given the cost as well as technical and legal challenges. Baugier describes the PMS platforms as "legacy APIs with documentation that is totally outdated" and considers Vero’s hard-fought integration to be a major moat.

But Propexo’s Okoruwa is looking to make that moat easier for others to cross. Propexo is building a unified API to allow tech companies to more easily integrate with multiple property management systems at once. "On average, proptech companies spend 20% of their engineering hours on PMS integration maintenance and management," stated Okoruwa. "We’re allowing [PropTech companies] to connect their apps with the most popular PMSs in the market in a consistent way."

Specifically, Propexo is an enablement technology rather than an intermediary; each Propexo client must have its own API credentials with each property management system. But Propexo provides its clients with a uniform API and standard data model, essentially translating the PMS platforms’ legacy systems into a more modern API with webhooks.

Like Vero, Propexo has a complicated relationship with the PMS platforms. "In some cases, we work hand-in-hand," says Okoruwa. "In other cases, it’s a bit more arms’ length as they don’t want intermediaries." But given that Propexo is simply providing code that its clients can use to expedite their own integrations—Propexo is not a third-party developer on PMS platforms itself—it’s unclear what levers PMS companies have to stop Okoruwa.

Baugier, however, is not a fan of Propexo. "I don’t like it. Selfishly, it minimizes the moat for our competition. We spent the money on our integrations, and we want others to spend a corresponding amount," said Baugier. "I went through that brain damage, I want everyone else to go through that brain damage."

But even with an enabling tool like Propexo, proptech point solutions have a fragile and uneasy relationship with PMS companies. "Platform players are both partners and competitors to best of breed software vendors, and that explains many strategic decisions," said Beveridge, sharing this anecdote:

Companies have long persevered with their PMS vendors' CRM apps. They are seldom excited about the technology, but changing CRMs is a big deal, so there was always a strong incumbency bias. That started to change a few years ago when some of the industry's biggest platforms started to move to best-of-breed providers. Cortland, Essex and Camden, for example, adopted Funnel.

Unsurprisingly, we have seen a variety of competitive responses. Yardi introduced transaction fees targeting marketing applications that integrate into its platform (such as Funnel). RealPage purchased Knock, another best-of-breed provider making inroads into legacy customer bases.

These examples highlight a fundamental threat facing proptech point solutions reliant on PMS integrations: the more successful they become, the more likely they are to draw attention—and retaliation—from their PMS partners.

Challengers and New Entrants

While Okoruwa looks to open up the existing platforms, others are looking to replace them entirely.

Jonathan Lonsdale, Founder & CEO of Ender, sees the property management system as the single biggest opportunity in proptech today. "The only non-marketplace multi-billion dollar companies in real estate tech are these accounting solutions," says Lonsdale. "But there are huge data issues because you have dozens of single point solutions that don’t talk to each other."

Rather than build a new point solution ("they either get shut off by Yardi or get bought," he explained), Lonsdale decided in 2018 to build a new PMS from the ground up. "Our end goal is to build an app store like Shopify," he says. "But to get to there, you need to solve all the use cases yourself. You need to be feature complete, have all the functionality, then other groups can plug into you."

While Lonsdale embraces openness, he is cautious about relying too much on third parties to provide core functionality. "We used RentLinx for a while to do syndication to the ILS—but then AppFolio bought them and shut them down for everybody else," Lonsdale recalled. "You have to build anything that’s core."

Lonsdale and his team have now been building for five years, and he described the scale of the challenge of building a PMS as follows:

There’s probably 10,000 workflows you need to solve for, and you’re not going to get credit for the first 9,000 or so. With 6,000 [workflows], people may use it but you have a shit product. At 9,000, maybe people can like it, but it’s missing major things—core accounting features and things that would be really helpful. But at 10,000, people love it when you add five new workflows.

While other startup PMS companies have focused on small, mom-and-pop landlords and operators—who have fewer requirements and simpler purchasing processes—Ender is tackling the heart of the PMS market with a product tailored to institutional owners. "Non-institutions and institutions are extraordinarily different," says Lonsdale. "If you have someone with a few hundred properties, [a user is] flying around the app, doing everything themselves. But if you have thousands of properties, you have one person just doing lease renewals, another doing accounting, and another doing AP."

Of course, serving institutions brings its own challenges. "No institution is going to use you unless another institution already uses you." Fortunately, Ender partnered with an institution—a large single-family buyer—early on and has been building the product with them ever since. "Once we’re stable, then we can go to market."

Lonsdale explained that he chose the single-family market as it was relatively underserved in the PMS space today. "RealPage and Yardi don’t work well with single family," Lonsdale noted. "But you can build the platform with a modern architecture that’s not too dissimilar from multifamily."

Like AppFolio’s Baird, Lonsdale is betting on workflow automation to differentiate his platform. "Our special sauce—if you get down to one thing—it’s internal integrations. If you structure all data in one system and sync communication in one system, you can automate more workflows and run reports."

Of course, Ender isn’t the only new company attempting to build a property management system from scratch. But it’s notable in that it is taking on the toughest segment of the market—institutional owners—rather than starting with small, mom-and-pop owners and operators who can more easily switch platforms.

The Emerging Incumbents

Not every incumbent PMS is relying upon its moat to maintain its market position. At least two large platforms are looking to take a more open and technology-forward approach.

With half a billion in capital from Silver Lake and a new leadership team, Entrata is a serious challenger in the institutional PMS category, investing heavily in new functionality. "Really what we’re doing is partnering with [our clients] on our product roadmap," said Fuhrman. "What should that look like? We have new tools in the toolbox from a development and M&A perspective for the first time in [our] history." Third-party analysts are similarly bullish on Entrata’s trajectory. "If there’s a player that’s likely to change things in the near term, it’s Entrata," noted multifamily expert Beveridge.

Despite additional resources, Entrata is solely focused on the rental housing sector. "Our market share is in student, conventional, active adult, military, and now affordable. When I start to look at any type of rental housing, we fall in that category. But we’re not going to be a Yardi and have a huge global office or industrial clientele. That commercial side isn’t part of our business," said Fuhrman.

Rather, Entrata is investing its resources in building out its core residential property management platform to better compete against industry incumbents. As highlighted earlier, a big part of that will involve convincing accounting teams to leave the familiar confines of Yardi. Per Fuhrman:

"Yardi has 30 years of building accounting software, we have just 10. We have a significant portion of our clients on our accounting platform, we have institutional clients and REITs who are pretty darn happy with it. We’re still building out components of it. We’ll have to continue to invest. But Yardi has the benefit of a lot of years ahead of others."

While accounting and reporting is a major objective at Entrata, it’s not the only one: they’re also investing in data to lay the groundwork for more AI. "We’ve hired a number of data scientists," noted Fuhrman. "And our advantage will be in that data ecosystem and what [clients] can do with it."

Like Fuhrman, AppFolio’s Baird is a relative newcomer to the PMS space. A veteran engineering leader, he was most recently an executive at C3.ai, Tom Siebel’s enterprise AI platform. And at AppFolio he has continued to push the platform toward broad adoption of AI as well as a relatively radical degree of platform openness (on the spectrum of PMS platforms). "Our decision to open the platform was very intentional," noted Baird. "People start proptech companies all the time, and we have this great basis for doing business on. We allow you to integrate in an easy manner, it’s very quick." To their platform’s credit, AppFolio doesn’t suffer from the API problems I laid out earlier: their API is REST, not SOAP, and API documentation is available publicly online.

Baird sees third-party apps as a key way to enhance functionality for AppFolio’s clients. "There is too much stuff connected to our property management systems for us to own all of it," said Baird.

Entrata’s Fuhrman is more circumspect in her view of platform openness. "It’s a balance between investing in your own product versus investing in API endpoint development," she said. "What’s the fine line of where you assign your own product resources? Every endpoint you expose takes development, […] and we have to consider risk-reward especially when you consider CCPA, GDPR, payment risk, and data breaches."

Some of this divergence may come down to Entrata and AppFolio’s respective client bases. Entrata’s more institutional target customers are likely much more concerned with risk and compliance than AppFolio’s core of SMB owners. And Entrata’s main competition in the institutional space—Yardi—is winning no awards for platform openness, giving Fuhrman and Entrata little reason to push the boundaries.

An Opening or a Dead End?

Despite all the interest in opening and/or disrupting the PMS ecosystem, there are good reasons to be bearish. "Yardi and RealPage have operated the way they have for 30 to 40 years," says Baugier. "Yardi is a $27 billion company owned by one man. The secret sauce they’ve come up with works, and I don’t think their approach to partnerships is going to change."

Baugier is not alone in his outlook. Our informal Twitter poll—which likely reached a fairly tech-forward audience—showed that a plurality believe that Yardi will still be the largest property management system in 2035, and almost 80% believe it will be one of the existing incumbents:

Others I interviewed are similarly bearish that the major PMS platforms will pivot to a more open approach. "You could imagine a formulation of an app store model where the PMS acts more like an integration layer into which users could plug applications," said Beveridge. "But someone else would probably have to build it rather than today's dominant platform providers."

Still, it is worth asking why real estate should be fundamentally different from other industries which have seen their ERP platforms embrace more open architectures and third-party partnerships over the past 20 years. Ultimately, those transformations were driven by clients demanding new functionality faster than the ERP providers were able to deliver it on their own. "Hubspot was never going to build a lot of the features these [third party] companies are offering," says Okoruwa. "Hubspot wanted to be the hub around which a lot of these tools connected."

But the complexity of real estate capital relationships may prove too much to surmount. After all, the people happily viewing Yardi and RealPage reports—asset managers at institutional owners and their bosses—aren’t the ones struggling with broken APIs or mediocre CRMs. "Everything that isn’t accounting has to be just good enough that the payback from switching to something else isn’t positive," says Beveridge.

In theory, asset owners could demand better from their PMS providers or threaten to migrate to platforms with a more open approach. But despite building owners—not PMS systems—owning the user and asset data within those platforms, switching platforms is not an easy task. "While [building owners] technically own the data, ownership is driven by the ease with which you can get the data out and share it," notes Okoruwa.

Beveridge, for one, believes that AI may finally shake up the PMS landscape. "If you’re in an environment where more than 70% of inbound calls are handled by robots, what is a CRM even for?" As AI—whether through a PMS like AppFolio or standalone tools—automates more tasks, the need for a complex PMS tool with multiple modules and human interfaces declines. "You have this software that everyone invests loads of time in rolling out, which is fundamentally about telling an ape what to do next at a property," says Beveridge. "It’s this system of workflows which says ‘this happened 2 days ago, now do this’." With more of these tasks automated, the "familiarity moat" which has historically protected PMS systems begins to evaporate.

"I hear that there may be a version of Quickbooks that will be ‘lights-out’ AI-enabled. If that is possible, how many accountants do real estate owners need? […]Technology is going to make the people [PMS platforms] rely on to stop competitors obsolete."

If property accountants have less power to protect an in-place PMS, other moats—such as standardized reporting packages—become easier to bridge. "REBA is doing best-in-class analytics," says Beveridge. "Do I optimize an Entrata-centric platform by saying that the data bit is being handled by a best in class platform [like REBA] alongside Entrata?"

But the ultimate winners in the PMS sector—and the level of openness they embrace—will come down to multifamily owners and how much they push for change. "We do what’s right for AppFolio and our customers," said AppFolio’s Baird. "We’re more focused on that than what the competition will do."

—Brad Hargreaves

Thank you for reading Thesis Driven. Know someone who should read this letter? Feel free to share it.

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them

Start Writing

Start Writing