Hot and Cold: Where Real Estate Tech Investors Want to Play in 2024

The results of Thesis Driven's biannual real estate tech investor survey

Over the past few weeks, we’ve surveyed almost 50 established real estate tech investors across a variety of stages and categories. Later this week, we’ll share details of specific investors and their favored categories, updating this list from six months ago—as well as each firm’s interest areas, ability to lead deals, recent investments, and PropCo involvement.

But today’s letter will focus on macro trends in investment interest: particularly, the sectors of real estate tech drawing the most interest from venture investors and real estate strategics today.

While 2023 was a down year for real estate tech investment—and venture at large—most investors believe that the market is on its way back. The majority of venture investors—approximately 65%—believe that 2024 will see more venture dollars deployed into real estate tech than in 2023. Only 16% believe that 2024 will see a continuation of declining deal volume.

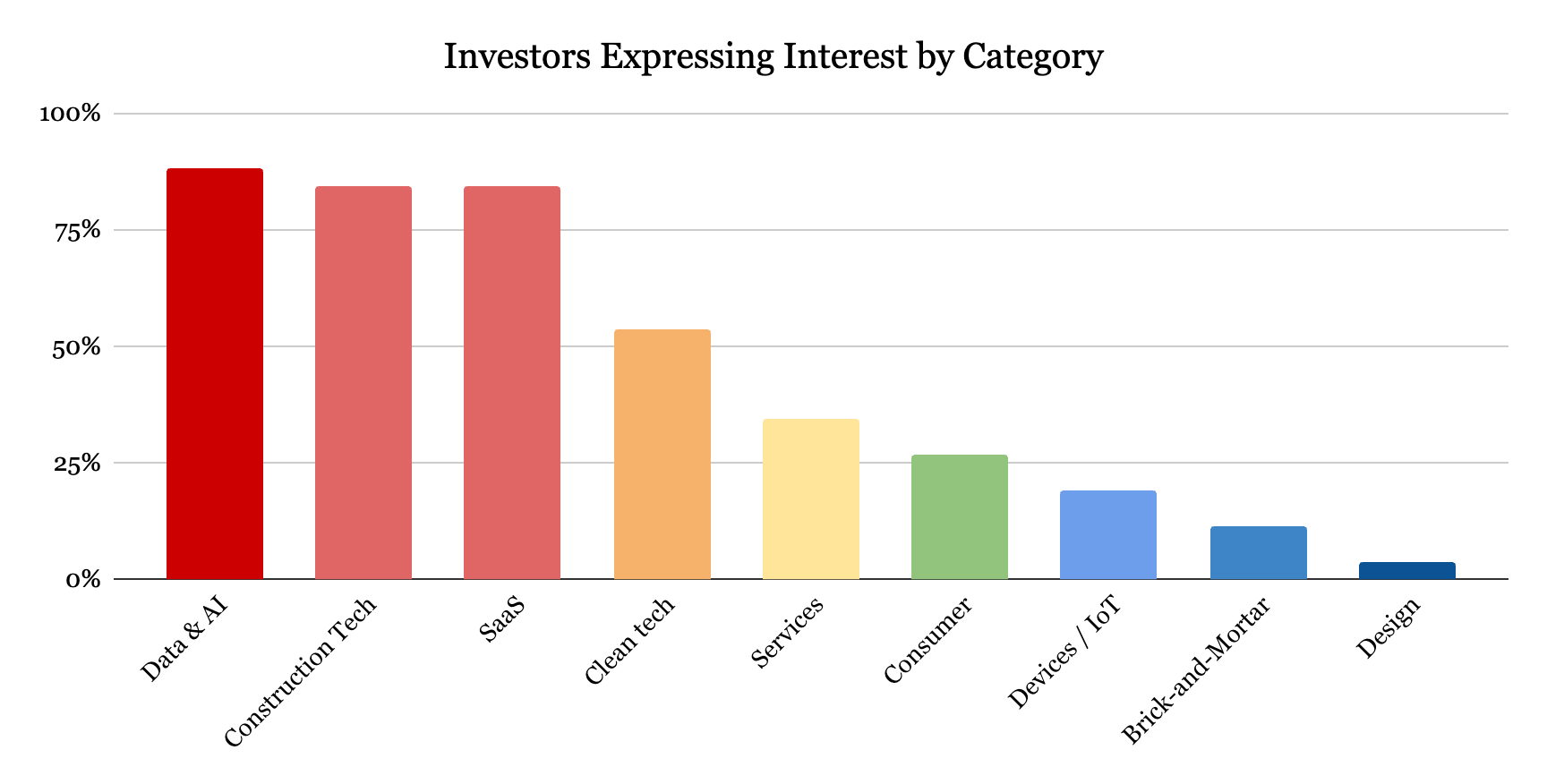

But the bullishness isn’t spread evenly across real estate tech categories. Data & AI and construction tech, for example, are hot categories, with the vast majority of investors looking to do more deals there. Brick-and-mortar businesses, on the other hand, are on the outs, forcing entrepreneurs to look for alternative financing paths.

Today’s letter will walk through each major subcategory of real estate tech—data & AI, brick-and-mortar, SaaS, design, services, consumer, devices / IoT, construction tech, and clean tech—and discuss how each is faring in the venture market and how companies in those sectors might approach the market.

According to CRETI, proptech companies raised a bit over $11 billion in 2023, a decline from 2022 and an even steeper drop from 2021’s highs. But the bleeding has likely stopped; Q4 saw a rebound in funding to levels not seen since the first half of 2022 as more investors left the sidelines.

But as noted above, the rebound was not evenly spread across proptech categories. While the CRETI report didn’t break investment down by sector, Thesis Driven’s survey identified the haves and have-nots across categories.

Let’s break each down from hot to not:

Scorching Hot

Data & AI

No sector drew more interest across the venture landscape in 2023 than data & AI, and real estate tech-related AI companies were no exception. AI-related startups raised almost $50 billion in venture capital in 2023, although much of that went to companies building foundational LLM technologies like OpenAI and Anthropic .

But real estate tech startups weren’t left out entirely. JLL estimated that $4 billion was raised to back AI-enabled proptech companies in 2022, with almost half invested in earlier-stage companies. 2023 also saw new financings for AI proptech names; leasing automation platform EliseAI raised $35 million in June and AI-enabled collections platform Colleen raised $3.5 million in July, to name a couple.

Of course, some investors wonder where the value created by the AI revolution will ultimately accrue. Will companies building core technologies take the bulk of the pie? Or will incumbents with built-in customer bases—such as AppFolio, which is heavily investing in AI tools—use their advantages to keep new entrants at bay? As we go into 2024, it’s often not enough to simply put a industry-specific wrapper on an LLM; startups must have a more defensible advantage. But investors are clearly paying close attention.

Construction Tech

Despite several high-profile startup failures over the past few years, construction tech remains an area of significant interest for venture investors. On the surface, the macro arguments for construction tech investment couldn’t be better:

Construction ranks at the bottom of technology adoption and digitization across industries;

Construction productivity has been more or less flat since the 1940s, a wild outlier among industries;

There is a severe construction worker shortage on the horizon with few good (and politically feasible) solutions, which will force many contractors and developers to embrace technology;

We’re not building enough housing in the places that need it.

Still, construction tech is devilishly hard, and just because there’s investor interest doesn’t mean checks will get written—investor capital still needs worthwhile concepts managed by credible founders to back.

Construction tech also differs from Data & AI in that it benefits from sector-focused investors solely interested in construction innovation. Zacua Ventures and Foundamental as well as strategics like CEMEX Ventures are primarily focused on the issues facing the construction industry rather than real estate tech writ large.

SaaS

Nobody ever got fired for investing in SaaS.

Of all sub-categories of proptech, Software-as-a-Service (SaaS) almost certainly generates the greatest deal volume, if not the highest dollar value invested. For one, generalist investors without any specific real estate experience can get behind vertical SaaS businesses serving the real estate industry as part of a broader thesis around vertical software—so it’s not rare to see SaaS investments in the sector from investors who don’t normally invest in real estate tech and therefore aren’t part of our survey.

But even among real estate tech-focused investors, SaaS remains a hot category, with over 80% of investors expressing interest. That said, VCs are likely to be far more discerning when evaluating SaaS companies than they were in the past. "Point solutions"—software tools that tackle a single aspect of the real estate value chain, for example, replacing a Yardi feature—will be viewed skeptically. But companies tackling big, thorny problems like building an entirely new property management system or launching an alternative data platform should continue to draw interest.

Overall, over 80% of the investors were surveyed were interested in new real estate-focused SaaS concepts.

Balmy

Clean Tech

Like AI, clean tech draws no shortage of attention and buzz—as well as capital. Real estate strategic investor Fifth Wall raised a $500 million climate fund in 2022, an indicator of institutional interest in the category as well as the tight relationship between real estate tech and climate tech.

As with construction tech, investing in climate tech is hard. But unlike the construction tech category—in which basic online tools still lack penetration—there aren’t many pure-play software paths to build a billion-dollar climate tech business. Most climate tech, after all, needs to touch the physical world in some form or fashion. This scares off a number of investors who prefer to make bets in the world of bits—even within real estate tech—and likely drove interest level down. (We’ll talk more about the very cold universe of brick-and-mortar later on). Ultimately, just more than half of the investors we surveyed expressed interest in clean tech.

But macro forces and credibility work in clean tech’s favor. While some later-stage generalist investors shy away from proptech entirely ("Do owners even want this stuff?"), clean tech has no such concerns. The value proposition of tech that works is clear, and governments on both sides of the Atlantic will happily subsidize the sector’s growth.

Services

Despite a reputation for low margins and long slogs, a number of real estate services companies—such as property management, cleaning, concierge, and brokerage—got venture backing over the past decade. And in pretty much all cases, those businesses lived up to the promise of a long slog with low margins.

The pandemic and real estate market roller coaster over the past few years put many of these businesses on life support. But even companies that got the timing right—single family property managers like Mynd, for example, riding the wave of institutional interest in SFR—showed that they are subject to market changes that can put growth on an indefinite pause.

But those are minor problems in comparison to the dreadful multiples at which real estate services businesses trade. It is not unreasonable for small services businesses to trade in the private market for 3-5X EBITDA, and large ones for 5-8X EBITDA. But not only did most venture-backed services businesses not have any EBITDA on which to base a multiple, they had often raised capital in excess of their closest (larger) comps’ entire market caps. In 2021, real estate brokerage Compass aimed for an IPO valuation of $9.7 billion despite generating half the revenue of its largest competitor, Realogy, which was valued at the time at $1.7 billion. (Today, Compass’s market cap is approximately $1.6 billion. )

While venture investors aren’t particularly enthused about real estate services right now, it’s hard to deny the need for better services businesses and the role that tech could play in making aspects of those services more effective and effective and efficient. And that’s why this category is here—merely balmy—rather than in the deep freeze.

Chilly

Consumer

In real estate tech, "consumer" refers to products and services—often branded—targeting end users. This can include branded real estate concepts like short-term rentals or fractional ownership (e.g., Pacaso) as well as consumer-oriented financial products like Better Mortgage.

Unfortunately, the tide has gone out on venture investing in consumer products and brands writ large. After a decade of high-profile venture investments in companies making new brands shoes, mattresses, and other retail products, the public markets soured on these companies’ eye-watering valuations and high burn rates. Now, many of yesterday’s consumer darlings are trading at orders-of-magnitude discounts off their highs. The air—and venture capital—has gone out of the consumer market.

But the market is still open for the right consumer business. After all, the most successful real estate tech company of the past decade, Airbnb, is a consumer marketplace. So it’s important to distinguish between companies building consumer products—which are having a tough run of it—and companies creating consumer-focused marketplaces or tools. There’s still a place for the latter, as is shown by recent venture rounds for real estate discovery platforms like Closing Theory and vacation rental platform Overmoon.

And while we didn’t break it out as a separate category, consumer fintech remains hot. The biggest proptech deal thus far this year was rental credit card rewards company Bilt’s $200 million equity round, handing the company a $3.1 billion valuation and placing former American Express CEO Ken Chenault on their board.

Devices & IoT

The contest of venture-backed disappointment is a close race between construction tech and internet-of-things (IoT). But IoT doesn’t have construction tech’s obvious macro tailwinds. Instead, real estate-oriented hardware devices face a number of daunting problems:

Building hardware is challenging. A number of things need to come together to make good hardware come to life, and the talent that can make it all happen is scarce and expense.

Value—and willingness to pay, especially among renters—is unclear. Ten years ago, many multifamily owners and developers believed that renters would pay more for apartments and condos loaded up with IoT devices. In general, those bets didn’t pan out, and many owners were stuck with devices with high maintenance costs and a short lifespan.

The incumbents are winning. IoT is actually happening in many ways, but almost all of it is being led by existing incumbents incorporating new, connected technology into their devices, leaving little room for startups to gain traction.

For a time, multifamily-focused smart lock producer Latch appeared to have reached escape velocity. But its post-SPAC existence could not have gone worse: restatements of financials, shareholder class action lawsuits, accusations of misrepresentation, and delisting from the NASDAQ for failing to meet its filing obligations.

While some investors remain curious about IoT’s potential, there is relatively little activity in this sector today.

Frozen Solid

Brick-and-Mortar

It shouldn’t be too surprising to see brick-and-mortar concepts on the outs among venture investors. It is, after all, hard to reconcile the pace of brick-and-mortar business growth—one location at a time and typically dependent upon the pace of construction—with the return expectations of venture capital.

That said, it’s certainly a departure from the easy money era of 2015-2021. For a time, WeWork—very much a brick-and-mortar concept—was the most valuable startup (real estate or not) in the entire US at $47 billion. But times change, and bringing a physical world concept to a VC investment committee is no longer a good way to get on the GP track. Barely 10% of the investors were surveyed were excited about new brick-and-mortar businesses.

This shift has opened the door for alternative investment models to gain traction among operators with novel stick-and-bricks businesses. Now that innovations in categories like hospitality, single-family rentals, industrial, and office can’t easily access the venture market, alternative funding sources like co-GP partnerships, OpCo-PropCo structures, and joint ventures make more sense. Many entrepreneurs are also likely to reformulate their businesses as investment managers, and real estate-focused accelerator programs like ReSeed are poised to benefit.

Design

While certainly not a popular investment category, "design" probably suffered from being a little too vague for most of the VCs we surveyed. While design services firms are unlikely to draw any investment interest, design-focused software tools have gained some traction.

Design optimization software company TestFit, for example, raised a $20M Series A led by Prologis Ventures in mid-2022. Other software tools touching the design process like Moderne-backed Tailorbird are also doing well. And generative AI-driven design tools like StageGlass are poised for growth as emerging technologies like NeRFs get better. So I don’t think it’s fair to say that design tech as a concept is less interesting than, say, brick-and-mortar. But the companies that will draw investors likely overlap with other categories here too.

Most investors believe proptech funding will bounce back in 2024, and last year’s strong Q4 hints that they are likely correct. But the windfall won’t be evenly distributed, and it certainly won’t look like the excesses of the pre-pandemic years. Just as some categories are en vogue, certain concepts are as well: strong unit economics, true technology moats, low burn rates, and solid gross margins. Companies with these traits are likely to do well regardless of where they sit.

Watch out later this week for our investor-by-investor deep dive.

—Brad Hargreaves

Recommend Thesis Driven to the readers of Devon's wanderings

A deep dive into emerging real estate themes and the innovators capitalizing on them